Strategic Insights Report: Battery Packs

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

INDEX

- Executive Summary

- Why Battery Packs? Why now?

- Battery Pack Anatomy & Value Chain Positioning

- Types of Battery Packs

- Indian Market Opportunity

- Target Segments & Customers

- Strategic Drivers

- Business Model Options

- Competitive Landscape

- Financials & Unit Economics

- Investments

- Certifications Required

- Call to Action

ㅤ

EXECUTIVE SUMMARY

ㅤ

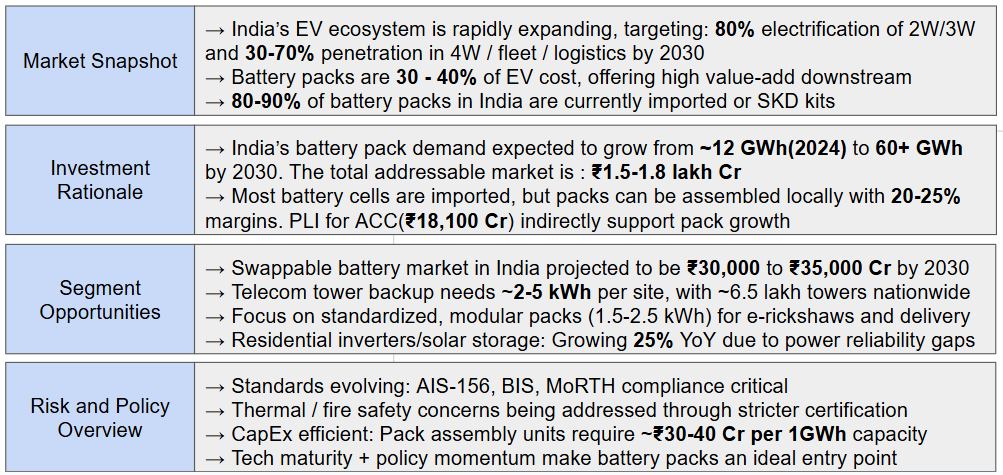

WHY BATTERY PACKS? WHY NOW?

ㅤ

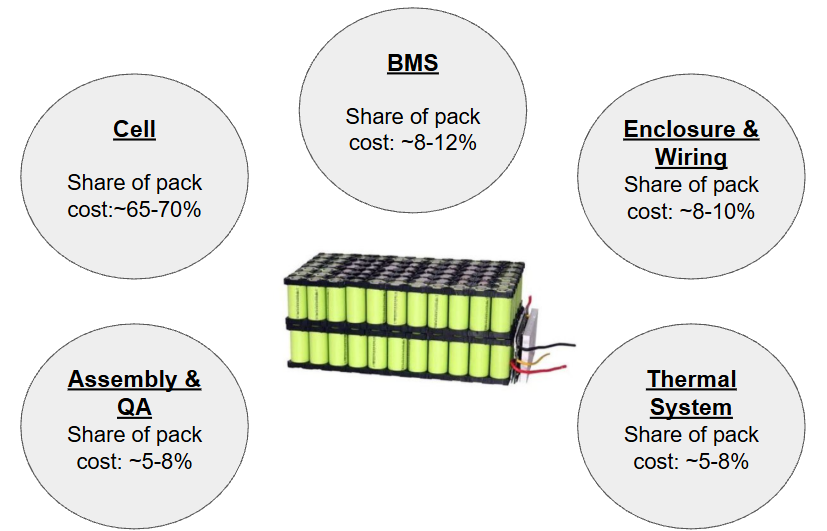

BATTERY PACK ANATOMY

ㅤ

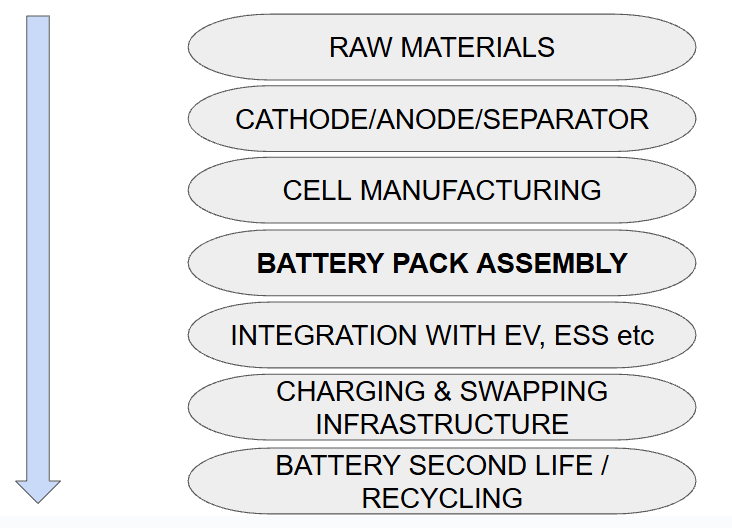

BATTERY PACK VALUE CHAIN POSITION

ㅤ

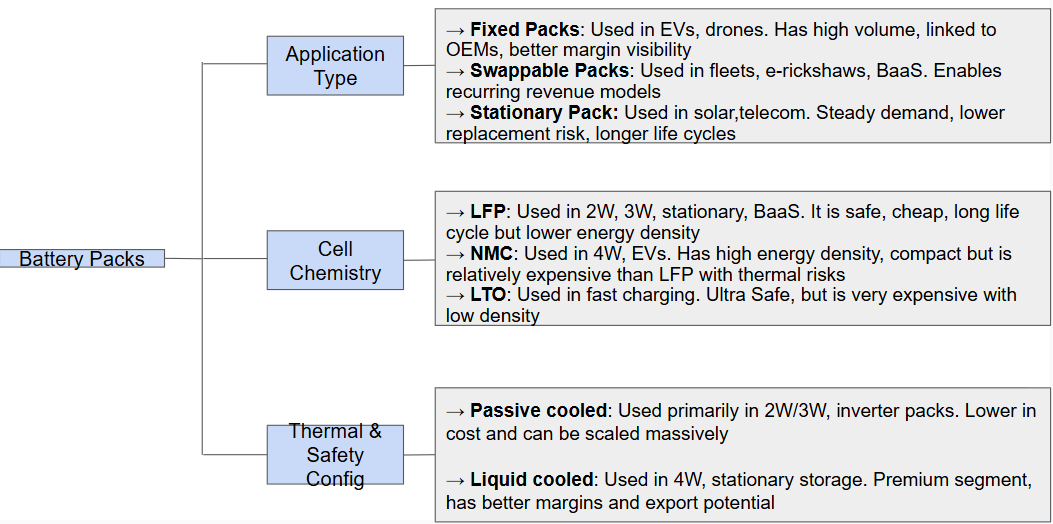

TYPES OF BATTERY PACKS

ㅤ

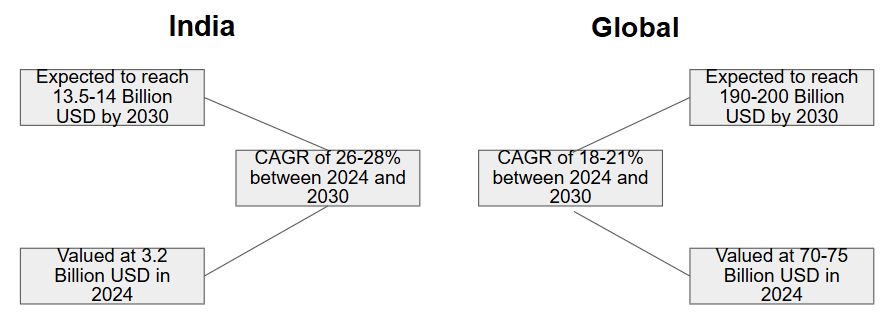

MARKET SIZE & PROJECTED GROWTH

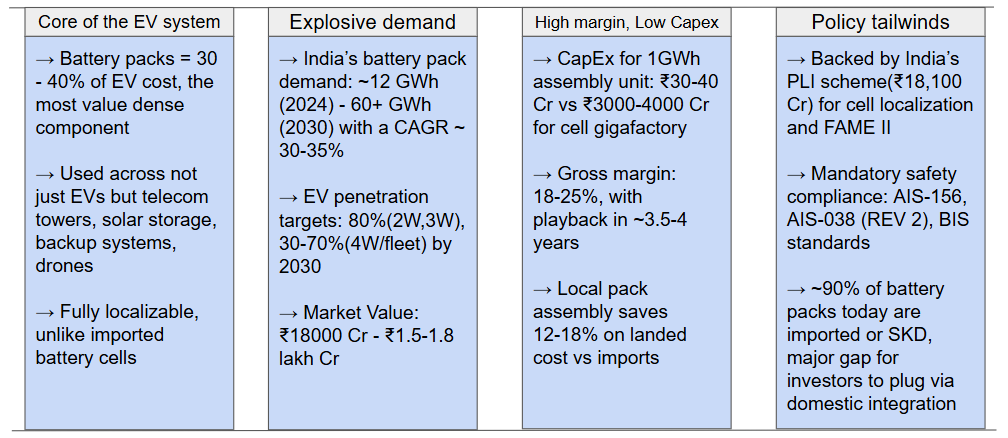

- Battery packs contribute ~30-40% of total EV cost, making them the most critical component in the electrification value chain.

- India’s market is growing 1.5x faster than the global average, offering an unmatched entry point for localized manufacturing and tech innovation

ㅤ

DEMAND BREAKDOWN BY SEGMENT

| Segment | Est. GWh Demand | Typical Pack Size | Notes |

|---|---|---|---|

| 2W / 3W EVs | 35–40 GWh | 2–7 kWh | Largest volume, LFP-based, localizable |

| 4W EVs / Fleets | 10–12 GWh | 15–30 kWh | Growth via fleets & urban delivery |

| Battery Swapping Infra | 5–7 GWh | 1.5–2.5 kWh | Fast-growing; requires modular packs |

| Stationary (Telecom, Solar, Backup) | 5–6 GWh | 2–10 kWh | Non-EV usage in power reliability |

| Industrial (Drones, AGVs) | <2 GWh | 1–3 kWh | Niche, but growing premium demand |

ㅤ

TARGET SEGMENTS & CUSTOMERS

| Segment | Est. Demand (2030) | Pack Size | ₹/kWh Cost | Key Customers | Investor Angle |

|---|---|---|---|---|---|

| 2W / 3W EVs | 35–40 GWh (~60–65%) | 2–7 kWh | ₹9,000–₹10,500 | Hero Electric, Ola, Ather, e-rickshaws | High volume, low CapEx, fast scaling |

| 4W EVs & Fleets | 10–12 GWh (~20–25%) | 15–30 kWh | ₹12,000–₹13,500 | Tata, Mahindra, BluSmart, Amazon, Flipkart | Premium segment, strict norms, higher ASP |

| Swapping / BaaS | 5–7 GWh (~10%) | 1.5–2.5 kWh | ₹10,000–₹11,500 | SUN Mobility, Battery Smart, Bounce | Recurring revenue, modular design advantage |

| Stationary Storage | 5–6 GWh (~8%) | 2–10 kWh | ₹9,500–₹11,000 | Jio, Airtel, solar EPCs, UPS vendors | Stable B2B demand, low churn |

| Drones & AGVs | <2 GWh (~2–3%) | 1–3 kWh | ₹14,000–₹16,000+ | ideaForge, Garuda Aerospace, robotics startups | Niche tech, high-margin, export opportunities |

ㅤ

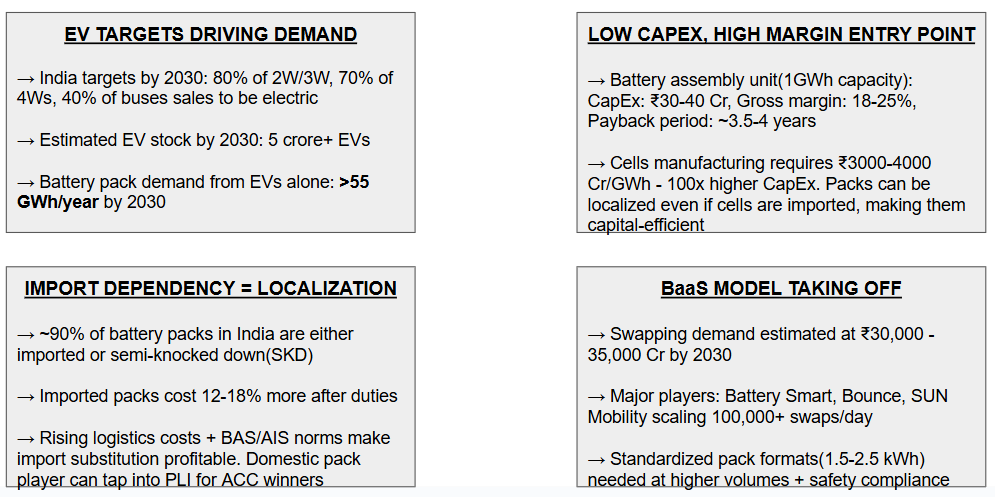

STRATEGIC DRIVERS

ㅤ

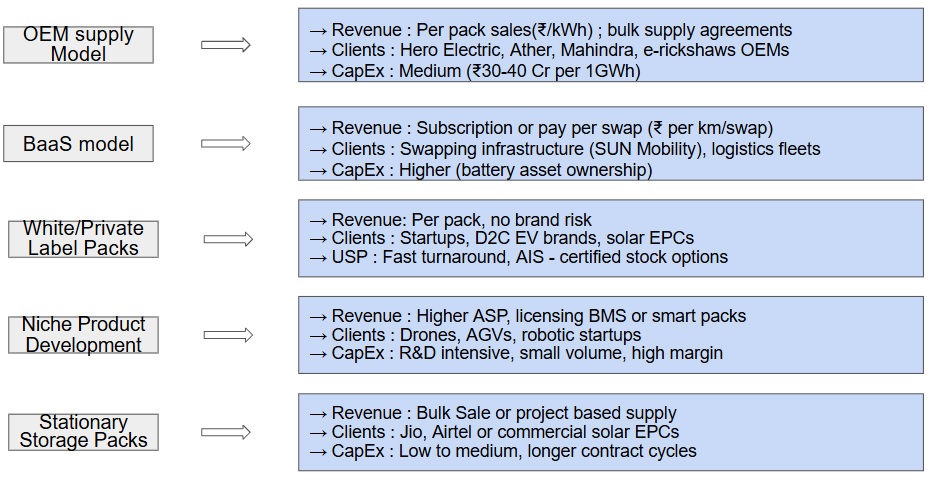

BUSINESS MODEL OPTIONS

ㅤ

COMPETITIVE LANDSCAPE

PACK MANUFACTURERS

| Player | Focus Segment | Strengths | Gaps / Notes |

|---|---|---|---|

| Okaya Power | 2W/3W packs, ESS | Scale, distribution | Limited BMS/IP, mostly standard packs |

| Nexcharge (Exide + Leclanché) | 4W, ESS | Backed by cell tech & JV | Premium-priced, B2B only |

| Trontek | 2W/3W packs | AIS-156 certified, large base | Mostly LFP, limited high-end IP |

| Livguard | Solar + telecom | ESS supply chain | EV entry still in mid-scale |

| Log9 Materials | BaaS, fast-charging packs | IP-driven thermal & BMS design | Still scaling, focused on ultra niche |

| EVage / others | Vehicle-specific packs | Integrated into vehicle design | Not open to third-party sales |

ㅤ

BATTERY SWAPPING

| Company | Key Offering | Battery Pack Dependency |

|---|---|---|

| SUN Mobility | Swapping infra + packs | Uses in-house + third-party pack suppliers |

| Battery Smart | Smart swapping platform | Outsources to AIS-156 pack vendors |

| Bounce Infinity | 2W EV + swapping | Builds + leases own packs |

ㅤ

CELL SUPPLY – IMPORT DEPENDENT

| Supplier | Presence in India | Used By |

|---|---|---|

| BYD (China) | Large LFP exports | Ola, Ather, Trontek, etc. |

| LG Chem | NMC/NCA cells (imported) | BluSmart, Mahindra |

| Panasonic | Premium 4W cells | Some 4W fleets |

| Reliance / Ola / Rajesh Exports | Gigafactories (PLI) by 2026+ | Domestic production incoming |

ㅤ

FINANCIALS & UNIT ECONOMICS

PER UNIT ECONOMICS(LFP PACK EX – 2W/3W)

| Metric | Value |

|---|---|

| Avg Pack Size | 2.5 kWh |

| Selling Price | ₹24,000–26,000 per pack |

| Cost of Goods Sold (COGS) | ₹18,000–20,000 |

| → Cell (60%) | ₹10,800–12,000 |

| → BMS + Assembly + Others | ₹7,000–8,000 |

| Gross Margin (₹) | ₹6,000–8,000 |

| Gross Margin (%) | ~25–30% |

| Warranty Provision | 5–7% of price |

ㅤ

ASSEMBLY PLANT FINANCIALS(1GWh)

| Cost / Revenue Head | Value (₹ Crore) |

|---|---|

| CapEx (Land, Equipment, Certs) | ₹30–40 Cr |

| Annual Output (packs) | ~400,000–450,000 (avg 2.5 kWh/pack) |

| Revenue at full capacity | ₹1,100–1,200 Cr / year |

| Gross Profit | ₹250–300 Cr / year |

| Operating Expenses (Opex) | ₹60–80 Cr / year |

| EBITDA | ₹170–200 Cr |

| EBITDA Margin | ~15–18% |

| Breakeven Period | 3.5–4 years |

ㅤ

RECORDED INVESTMENTS

| Investor | Technology | Investment Size | Capacity | Location |

|---|---|---|---|---|

| OLA Electric | Cell + BMS + Pack | ₹7,614 Cr | 20 GWh | Tamilnadu |

| Exide | Cell + Pack Assembly | ₹6,000 Cr | 6 GWh | Gujarat |

| Amara Raja Batteries | Li-ion Cell + Pack R&D | ₹9,500 Cr | 16 GWh by 2030 | Telangana |

| Reliance | Cell + BMS + Full Pack Stack | ₹10,000+ Cr | 20 GWh by 2036 | Gujarat |

| Lucas-TVS & 24M JV | SemiSolid Li-ion Cell + Packs | ₹3,000 Cr | ~10 GWh (target) | Tamilnadu |

ㅤ

CERTIFICATIONS REQUIRED

| Certification / Approval | Purpose / Issued By |

|---|---|

| CPCB Registration | Central authorization for recyclers & refurbishers |

| SPCB Consent (CTO + CTE) | Mandatory for operating recycling facilities |

| AIS 156 / AIS 038 Rev. 2 | EV battery safety standards (for traction batteries) |

| BIS (IS 16046:2018) | Mandatory for lithium-ion cell and pack safety compliance |

| ISO 14001, ISO 45001 | Environmental and occupational safety certifications |

| EPR Portal Compliance | Producers must report battery flows & recovery online |

| Fire & Safety Clearance | Required for storing and processing lithium battery packs |

ㅤ

MOVING FORWARD

Invest in a rapidly scaling market as India’s battery pack demand is projected to exceed 80 GWh by 2030, driven by surging EV adoption and energy storage needs.

Seize first-mover advantage in a fragmented ecosystem with limited availability of AIS-156-certified, modular, and intelligent battery packs.

Leverage strong policy and demand tailwinds, including FAME II incentives, PLI schemes, and rising fleet electrification in logistics and last-mile delivery.

Enter a high-margin, low-CapEx segment with gross margins of 15–18%, asset-light operations, and a breakeven potential in under 4 years.

Unlock multi-sector scalability by targeting 2W/3W OEMs, BaaS operators, solar/telecom backup markets, and export-ready tech for drones and robotics.

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in