Strategic Insights Report: Battery and Solar Panel Recycling

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

ㅤ

INDEX

- Executive Summary

- India’s Dual Waste Crisis

- Addressable Market & Material Recovery Potential

- Technology Stack

- Competitive & Infrastructure Landscape

- Unit Economics

- Regulatory Tailwinds

- Business Model (Two-Pronged)

- Recorded Investments

- Risk Mitigation

- Call to Action

ㅤ

EXECUTIVE SUMMARY

ㅤ

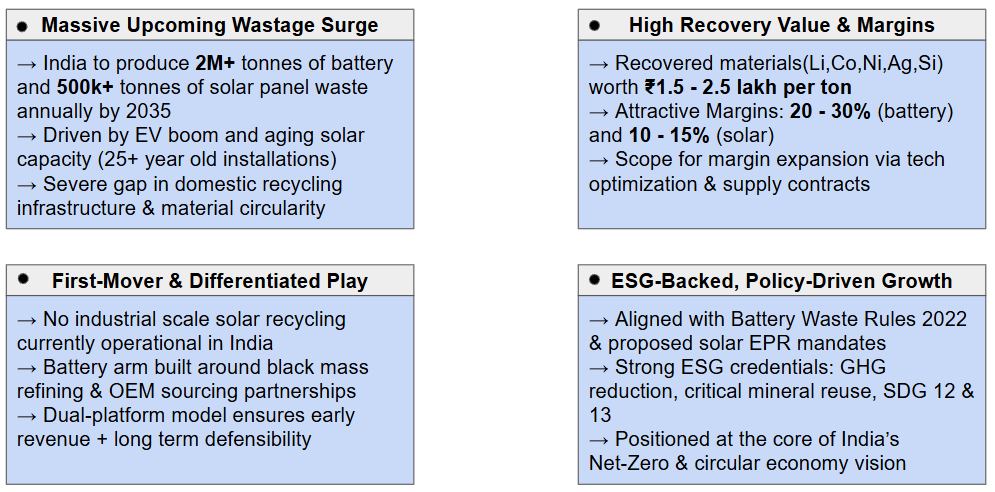

INDIA’S DUAL WASTE CRISIS

→ India had over 3 million electric vehicles on the road as of 2024 and is expected to reach 100 million EVs by 2030

→ A typical EV battery lasts 6-8 years, leading to a sharp rise in end-of-life batteries from 2025 onwards

→ India is projected to generate 5-6 lakh tonnes of used lithium ion batteries annually by 2030, rising to over 2 million tonnes by 2035

→ Current recycling capacity in India is under 15% of required capacity; most batteries end up in informal or unregulated sectors

→ India has installed over 80 GW of solar capacity (2024), targeting 280 GW by 2030

→ Panels have a lifespan of ~25 years → early installations (2000-2010) are approaching end-of-life

→ India will generate:

- 200,000+ tonnes/year of solar PV waste by 2030

- Over 1.8 million tonnes cumulatively by 2035

→ Majority are polycrystalline silicon panels with valuable components: glass, aluminium, silicon, silver

ㅤ

ADDRESSABLE MARKET (BATTERY)

WASTE VOLUME FORECAST

MATERIAL RECOVERY VALUE

→ Average black mass yield : ~35 – 40%

→ Recoverables : Lithium, Cobalt, Nickel, Manganese, Graphite

→ Gross recovery value : ₹1.5 – 2.5 lakh/ton (depending on chemistry and process)

MARKET SIZE ESTIMATE

ㅤ

ADDRESSABLE MARKET (SOLAR PANEL)

WASTE VOLUME FORECAST

MATERIAL RECOVERY VALUE

→ Key materials : Glass (~70%), Aluminium (~10%), Silicon (~5%), Silver (~0.05%)

→ Gross recovery value : ₹15,000 – 30,000 / tonnes

→ Tin, being in small quantities, has high market value and contributes to total recovery efficiency and resale margin

MARKET SIZE ESTIMATE

ㅤ

MATERIAL RECOVERY POTENTIAL – BATTERIES

| Material | Approx. % by weight | Avg. Recovery Rate (%) | Market Value (₹/kg)* | Recovered Value (₹/ton) |

|---|---|---|---|---|

| Lithium (Li) | 1.5–2% | 85–90% | ₹2,000–3,000 | ₹30,000–54,000 |

| Cobalt (Co) | 5–15% (in NMC) | 90–95% | ₹3,500–5,500 | ₹175,000–225,000 |

| Nickel (Ni) | 5–10% | 80–90% | ₹1,200–1,800 | ₹48,000–72,000 |

| Manganese (Mn) | 5–10% | 70–80% | ₹200–300 | ₹7,000–10,000 |

| Graphite | 10–20% | 60–70% | ₹50–100 | ₹3,000–5,000 |

| Copper, Aluminum | 15–20% | 90–95% | ₹600–800 | ₹75,000–100,000 |

ㅤ

MATERIAL RECOVERY POTENTIAL – SOLAR PANELS

| Material | Approx. % by weight | Avg. Recovery Rate (%) | Market Value (₹/kg)* | Recovered Value (₹/ton) |

|---|---|---|---|---|

| Glass | ~70% | 90–95% | ₹2–5 | ₹1,400–3,300 |

| Aluminum Frame | ~10% | 95–98% | ₹180–250 | ₹16,000–24,000 |

| Silicon (Cell) | ~5% | 80–85% | ₹250–300 | ₹10,000–12,750 |

| Silver | ~0.05% | 95%+ | ₹75,000–85,000 | ₹3,750–4,250 |

| Copper (Wiring) | ~1–2% | 90% | ₹700–800 | ₹14,000–16,000 |

| EVA & Plastics | ~10–15% | ~0–10% (low value) | Negligible | Negligible |

ㅤ

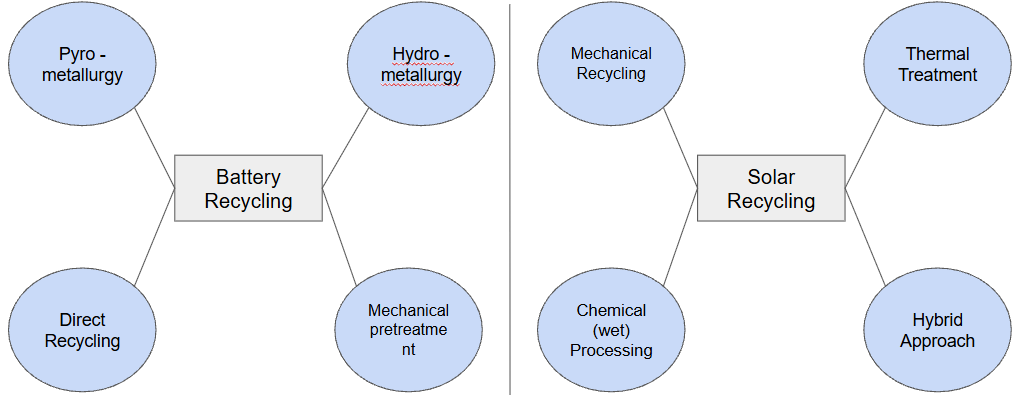

TECHNOLOGY STACK

ㅤ

COMPETITIVE LANDSCAPE (BATTERY)

| Company | Focus | Tech Stack | Scale | Positioning |

|---|---|---|---|---|

| Attero Recycling | Li-ion + e-waste | Pyro + Hydro (98% recovery) | 11,000 TPA (India), targeting 300,000 TPA globally | Market leader, large-scale, export-ready |

| LOHUM Cleantech | Li-ion + second-life | Direct recycling + repurposing | 1 GW recycling, 300 MW reuse | Tech-focused, circular value chain |

| RecycleKaro | Nickel recovery from Li-ion | Clean Ni-refining + thermal | 1,200 TPA Ni | Niche nickel player, vertical specialization |

| LICO Materials | Hydrometallurgical Li-ion recycling | ZLD Hydrometallurgy | 4 GWh → 10 GWh scalable | Green chemistry + scalable design |

| Tata Chemicals | Pilot Li-ion recycling | Wet chemistry R&D | ~500 TPA (pilot) | R&D player, early mover from chemicals side |

ㅤ

INFRASTRUCTURE LANDSCAPE

| Aspect | Current Status (India) |

|---|---|

| Authorized Recyclers | 30+ CPCB-registered recyclers (only 6–8 at industrial scale) |

| Installed Capacity | ~30,000–35,000 TPA (Li-ion specific), rising fast |

| Technology Readiness | Hydrometallurgy + direct recycling gaining traction; pyro being phased out slowly |

| Collection & Reverse Logistics | Fragmented; OEM tie-ups exist (Tata, Ola, MG, etc.) but lack of aggregation hubs |

| Policy Alignment | Strong post Battery Waste Management Rules 2022 (EPR model) |

ㅤ

COMPETITIVE LANDSCAPE (PANELS)

| Entity / Initiative | Focus | Tech Stack | Stage | Positioning |

|---|---|---|---|---|

| Attero + NISE (MoU) | Pilot recycling of PV modules | Mechanical + thermal + R&D | Pilot | Early mover in formal module recycling |

| Varanashi Farms (Surya Arka) | Upcycling waste solar panels | Manual + modular reuses | Pilot | Innovative repurposing |

| ReNew Power (BII-backed) | Module mfg with closed-loop design | End-of-life reuse planning (TBD) | Under planning | Backed by $100M for circular economy |

ㅤ

INFRASTRUCTURE LANDSCAPE

| Aspect | Current Status (India) |

|---|---|

| Formal Recyclers | 0 commercial-scale operators; 2–3 pilot initiatives (e.g., Attero-NISE, Varanashi) |

| Policy Support | Draft solar EPR guidelines in progress (expected 2025), part of CPCB Renewable Waste Act |

| Reverse Logistics | Missing; EPCs typically abandon/reuse panels informally |

| Processing Tech Readiness | Mechanical disassembly feasible; silver/silicon extraction still R&D stage |

| Waste Volume Forecast (2030) | ~600,000 tonnes (per CEEW); huge volume with no recycling capacity in place |

ㅤ

UNIT ECONOMICS

| Metric | Battery Recycling | Solar Panel Recycling |

|---|---|---|

| Avg. Revenue / Ton | ₹2,00,000 | ₹20,000 |

| Avg. OPEX / Ton | ₹85,000 | ₹20,000 |

| EBITDA / Ton | ₹1,15,000 | ₹0 – ₹8,000 |

| EBITDA Margin | 25% – 40% | -5% – 20% |

| Breakeven Volume (annually) | ~500–700 tonnes | ~2,000–3,000 tonnes |

| Scalability | Medium to High | Medium (needs tech upgrade) |

| Capital Intensity | High (₹15–20 Cr/plant) | Medium (₹5–8 Cr/plant) |

ㅤ

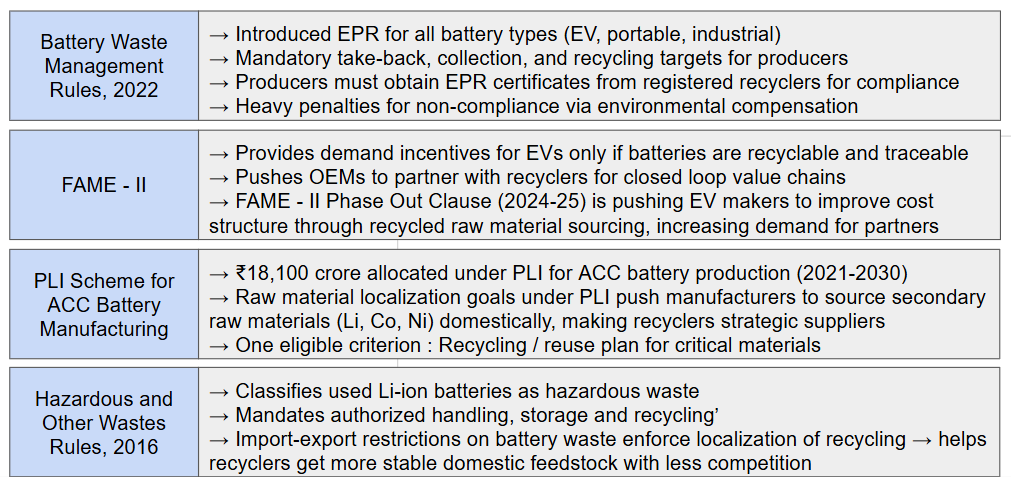

REGULATORY TAILWINDS (BATTERY)

ㅤ

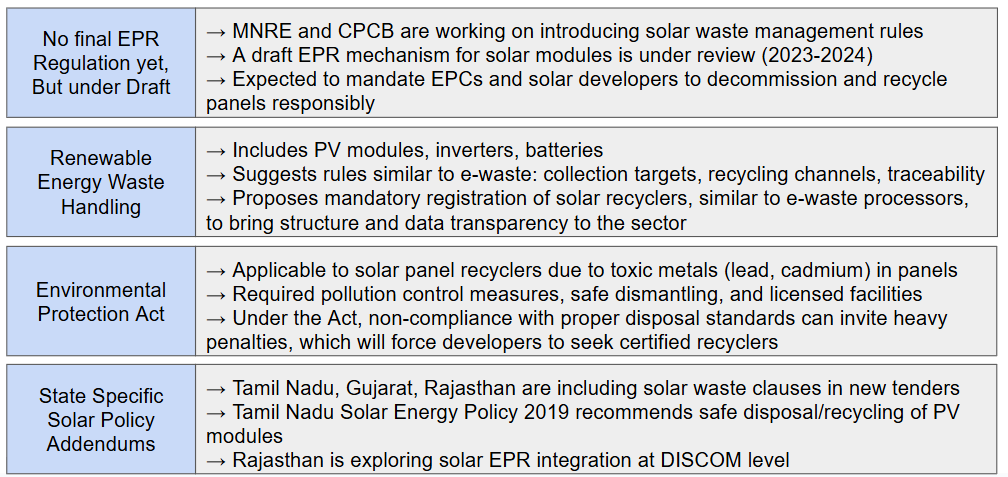

REGULATORY TAILWINDS (SOLAR)

ㅤ

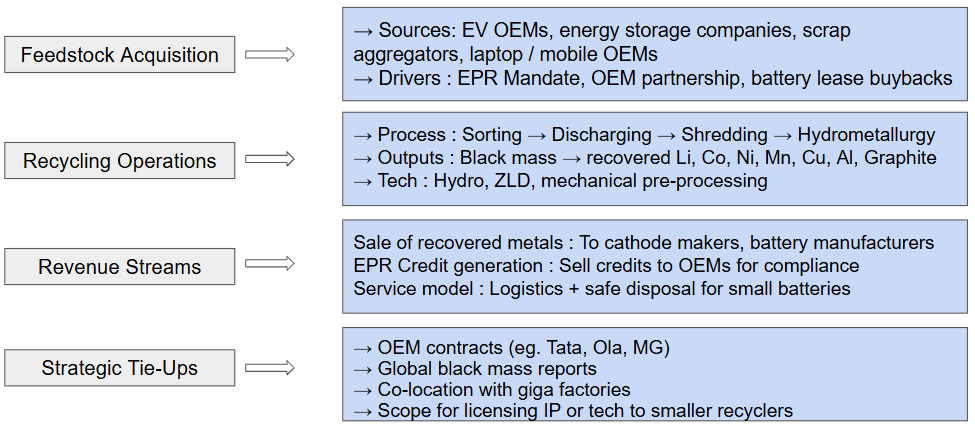

BUSINESS MODEL (BATTERY)

ㅤ

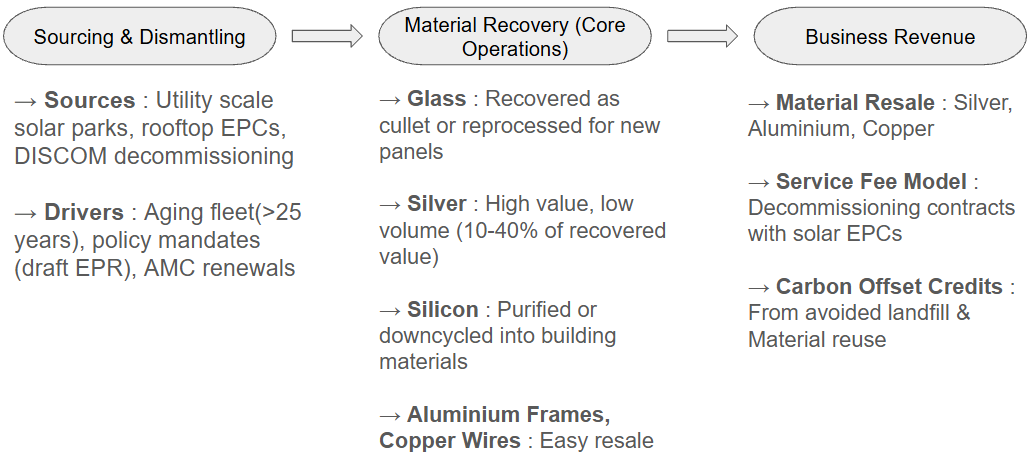

BUSINESS MODEL (SOLAR)

ㅤ

RECORDED INVESTMENTS

| Investor / Company | Technology / Focus | Investment Size | Capacity | Location |

|---|---|---|---|---|

| Attero Recycling | Li-ion battery recycling (Pyro + Hydro) | ₹300 Cr (~$36M) | 11,000 TPA | Noida, Uttar Pradesh |

| _ | Expansion (Phase II) | ₹600 Cr (~$72M) | 19,500 TPA | Telangana |

| _ | Global Scale | $1 Billion (~₹8,200 Cr) | 300,000 TPA (by 2027) | India, Europe, US |

| LOHUM Cleantech | Battery recycling & repurposing | $100 Million (~₹824 Cr) | 1 GW recycling + 300 MW second-life | Greater Noida, India |

| LICO Materials | ZLD hydrometallurgy | ₹250 Cr | 4 GWh (~17,500 TPA), scalable to 10 GWh | Bengaluru, Karnataka |

| RecycleKaro | Nickel extraction from Li-ion batteries | ₹100 Cr | 1,200 TPA Ni (input ~3–4k TPA) | Palghar, Maharashtra |

| Tata Chemicals | Pilot battery recycling | ₹10–20 Cr (est.) | ~500 TPA | Maharashtra |

ㅤ

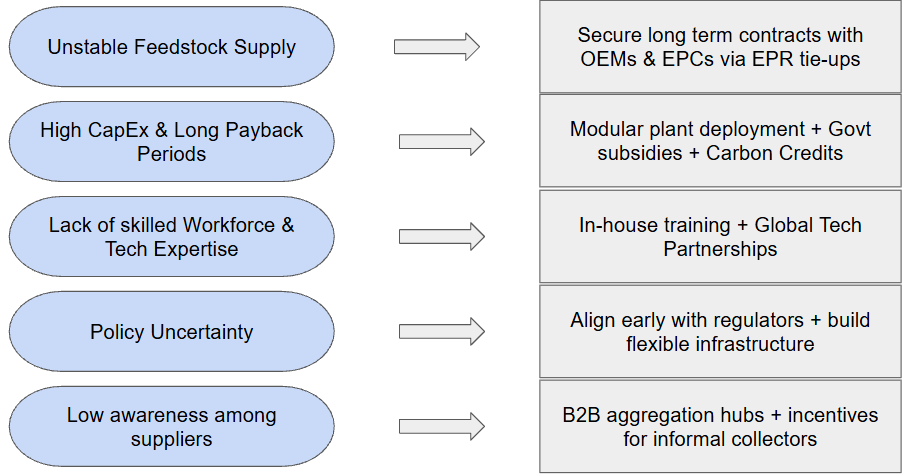

RISK MITIGATION

ㅤ

MOVING FORWARD

- Partner with us to establish India’s most scalable and efficient battery and solar panel recycling infrastructure

- Be an early mover in a circular economy sector backed by evolving regulations, strong material demand, and ESG priorities

- Capitalize on rapidly growing waste volumes by enabling sustainable recovery of critical raw materials like lithium, cobalt, silver, and silicon

- Help build decentralized recycling hubs across solar- and EV-heavy states, creating localized impact and national reach

- Leverage Extended Producer Responsibility (EPR) mandates to unlock long-term contracts with OEMs and solar EPCs

- Invest in clean-tech innovation driving zero-waste, high-yield recycling technologies with export potential

- Shape India’s transition to net zero by closing the loop on green energy technologies through smart resource recovery

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in