Strategic Insights Report: Solar Modules

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

INDEX

- Executive Summary

- Essential Drivers

- Market Overview

- Technology Landscape

- Manufacturing in India

- Policy & Regulatory Environment

- Cost & Financial Metrics

- Investment Potential

- Supply Chain Analysis

- Risk & Challenges

- Sustainability & Circular Economy

- Strategic Outlook

- Conclusion

EXECUTIVE SUMMARY

ㅤ

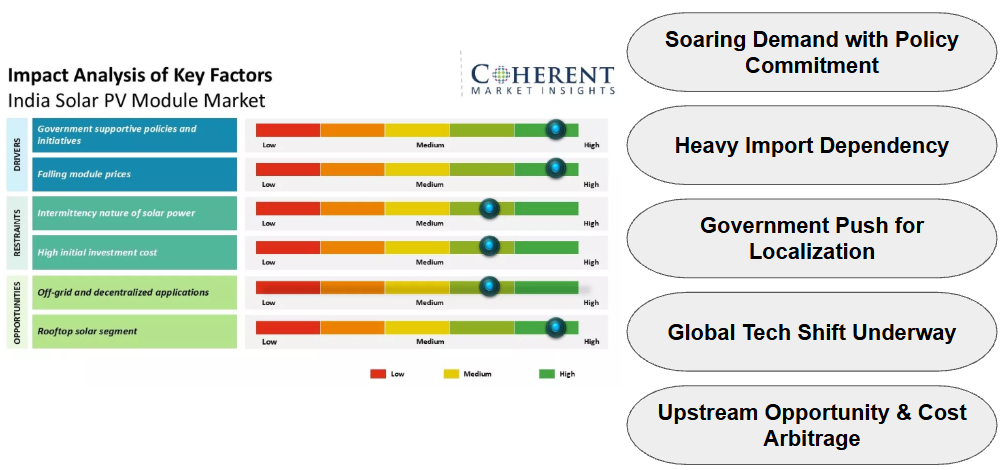

ESSENTIAL DRIVERS

ㅤ

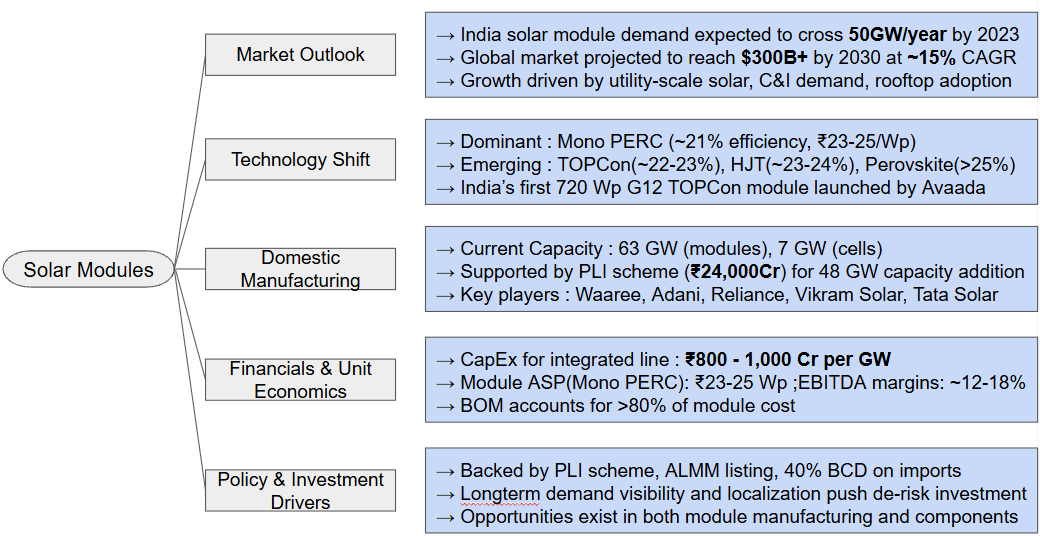

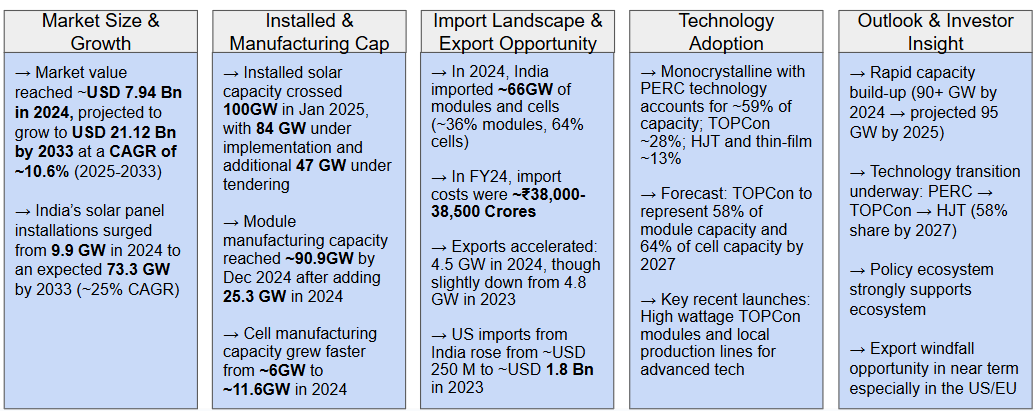

MARKET OVERVIEW

“With 50+ GW of annual demand and rising import risks, local module manufacturing is no longer optional – it’s inevitable”

ㅤ

TECHNOLOGY LANDSCAPE

| Tech | Efficiency | CAPEX ($/GW) | OPEX | Key Strengths | Challenges & Market Position |

|---|---|---|---|---|---|

| Mono PERC (baseline) | ~21–23.5 % | Retrofittable | Standard | Lowest cost (~$0.18–0.20/W); proven track record | Efficiency nearing theoretical max; supply tapering |

| TOPCon | ~23–24 % (lab >25 %) | ~$40 M/GW | Moderate, ~70–80% lower than HJT | Better temperature & degradation resilience; compatible with existing lines | Minor CAPEX/OPEX increase; initial defect risks |

| HJT | ~24–26 %, record ≥25.44 % | ~$70 M/GW | ~2.5× TOPCon | Highest potential yield, bifacial gain, longevity | High cost premium (25–30% higher ASP); financing skepticism |

| Bifacial Modules | +10–30% yield gains | Moderate premium | Slightly higher | Dual-sided generation ideal for trackers | Project‑specific; requires reflective albedo |

| Thin-film (CdTe/CIGS) | ~15–20% | Moderate–High | Lower | Flexible applications | Limited use, niche cases |

ㅤ

ECONOMIC CONSIDERATIONS

→ CapEx Trends: PERC lines retrofit cheaper than newer tech; TOPCon adds ~$40M/GW; HJT ~3x more than TOPCon

→ ASP & Cost per Watt:

PERC : $0.18-0.2/W

TOPCon : $0.22-0.25/W ($0.6-$1/W over PERC)

HJT : $0.3-0.35/W (25-30% ASP premium)

→ Year-1 degradation: PERC ~2%, TOPCon ~1%, HJT minimal

→ TOPCon: better thermal coefficient (~ -0.3%/oC) vs PERC(~ -0.35%)

→ HJT: best durability, near full bifacial output, 30+ year lifespan

→ India outlook : PERC’s market share dominates (~59%), TOPCon ~28%, HJT emerging

→ Major move to PLI-backend TOPCon & N-type bifacial (~715 Wp G12 by HVR Solar)

ㅤ

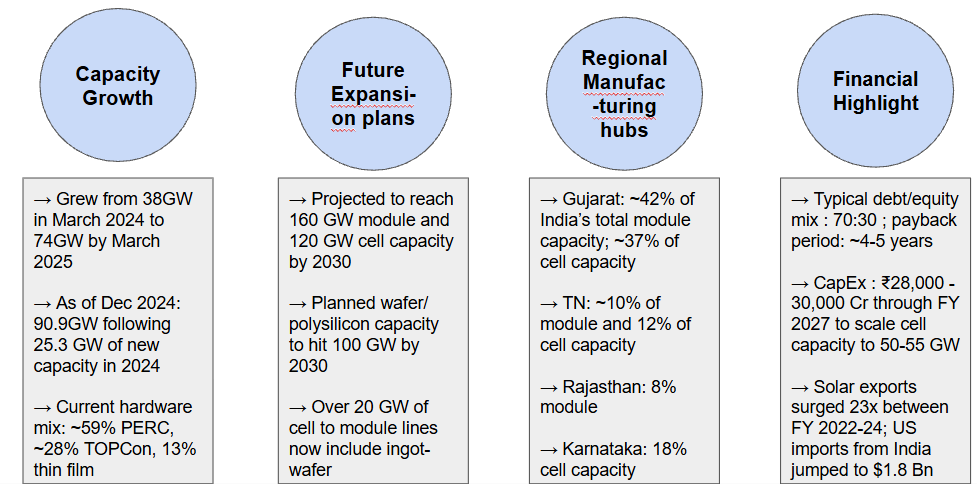

MANUFACTURING IN INDIA

ㅤ

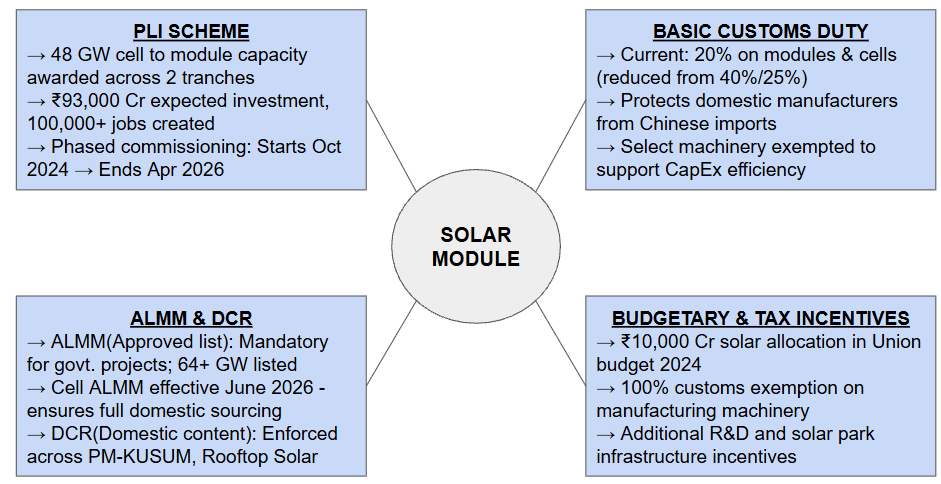

POLICY & REGULATORY ENVIRONMENT

ㅤ

COST AND FINANCIAL METRICS

| Metric | Value / Range | Investor Insight |

|---|---|---|

| CapEx – Integrated Fabrication | ₹3,200 Cr per GW (~US$400M/GW) | Enables upstream control and higher margin stability |

| CapEx – Module-Only Line | ₹250 Cr per GW | Lean entry with faster payback and lower complexity |

| CapEx – Cell-Only Line | ₹600 Cr per GW | Critical step for vertical integration and value capture |

| BOM Cost Share | Cell: ~60%, Other BOM (glass, EVA, etc.): ~32% | Cell manufacturing offers maximum cost leverage |

| Overheads & Labor | 3–5% of total module cost | Operational efficiency gains amplify margin as scale increases |

| Typical EBITDA Margin | 12–13% for integrated players | Strong profitability compared to global benchmarks |

| Payback Period | 4.5–5 years at ~50% capacity utilization | Attractive lifecycle for infrastructure-class investments |

ㅤ

MAJOR INVESTMENTS

| Investor / Company | Technology | Investment Size | Annual Capacity | Location | Notes |

|---|---|---|---|---|---|

| Avaada Electro | TOPCon (720 Wp G12 modules) | ₹13,000 Cr | 1.5 GW → 7 GW by Jul 2025 | Butibori, Nagpur (MH) | India’s first 720 Wp module plant |

| Reliance Industries | HJT + integrated PV + storage | ₹75,000 Cr | 10 GW initial, scaling to 20 GW | Jamnagar, Gujarat | Part of Mega Giga Complex |

| Emmvee Group | TOPCon + Mono PERC modules/cells | ₹15,000 Cr capex | 6.6 GW modules, 2.5 GW cells | Sulibele, Bengaluru (KA) | Opened 2 GW plant in Apr 2025 |

| Vikram Solar | N‑Type TOPCon (cell + module) | $200 M via DFC debt | 3 GW (expanding) | Tamil Nadu | DFC-backed facility |

ㅤ

SUPPLY CHAIN ANALYSIS

The Solar Modules value chain spans five core segments, each with its own growth dynamics and investment attractiveness:

ㅤ

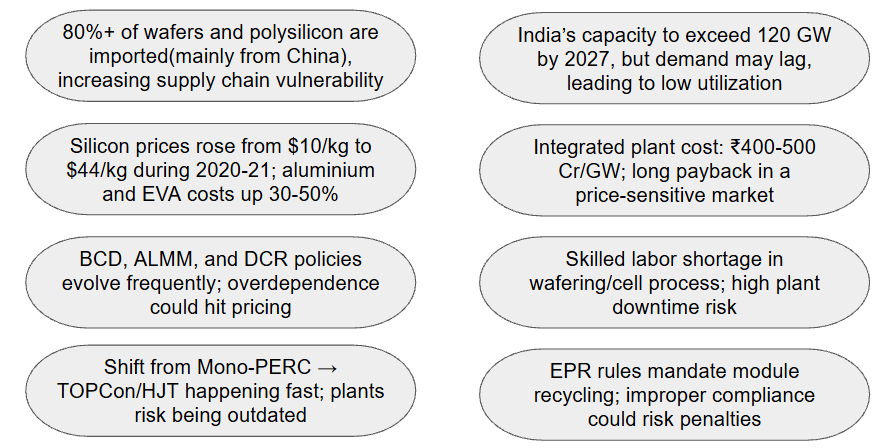

RISKS

ㅤ

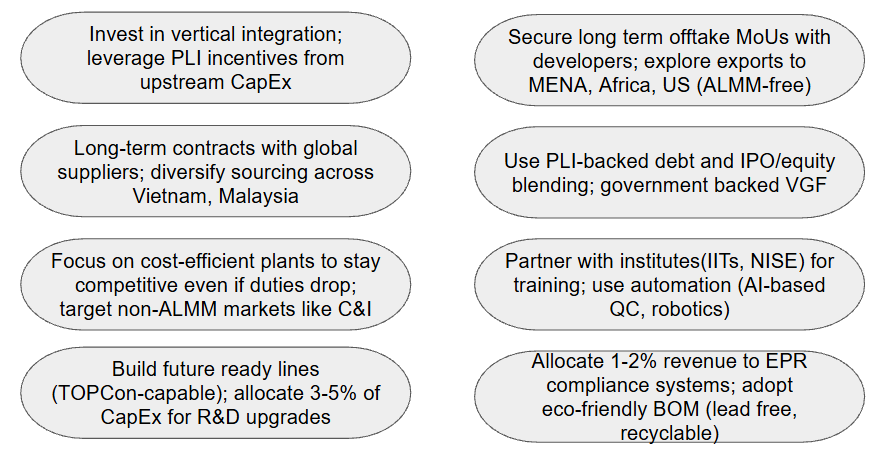

MITIGATION

ㅤ

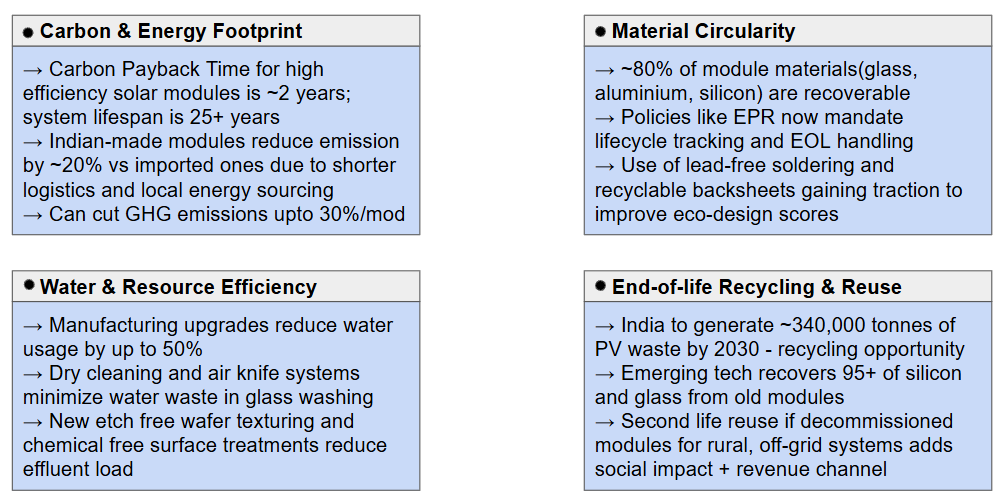

SUSTAINABILITY & CIRCULAR ECONOMY

ㅤ

STRATEGIC OUTLOOK

- India is positioning itself as a major global hub for solar module manufacturing.

- Strong government policy support is creating long-term industry stability.

- The market is shifting rapidly toward high-efficiency and future-ready technologies.

- Vertical integration is emerging as a key competitive advantage for manufacturers.

- Export opportunities are expanding, especially in markets diversifying from China.

- Sustainability and circular economy practices are becoming core business drivers.

- Early entrants are gaining first-mover benefits in capacity, incentives, and contracts.

- The sector offers a compelling risk-reward profile for long-term infrastructure investors.

MOVING FORWARD

India’s solar module manufacturing sector stands at a pivotal inflection point — backed by clear policy direction, growing domestic and export demand, and an industry-wide shift toward advanced technologies.

For investors, this presents a timely opportunity to participate in a fast-scaling market with increasing self-reliance, rising margins through integration, and ESG-aligned growth potential.

Strategic early investments in manufacturing capacity, innovation, and circular practices will not only generate competitive returns but also contribute meaningfully to India’s clean energy transition.

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in

India Big Business Opportunities in Climate Tech – List – EAI

India Big Business Opportunities in Climate Tech – List – EAI