Strategic Insights Report: Compressed Biogas (CBG)

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

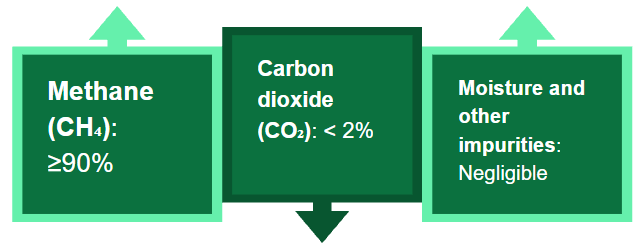

Introduction To CBG

Compressed Biogas (CBG) is a purified form of biogas that has been compressed to a high pressure (usually 200–250 bar) so that it can be used as a fuel similar to Compressed Natural Gas (CNG). It is produced from organic waste materials such as agricultural residue, animal dung, municipal solid waste, sewage, and food waste through a process called anaerobic digestion.This composition makes it nearly identical to CNG in energy content and combustion characteristics.

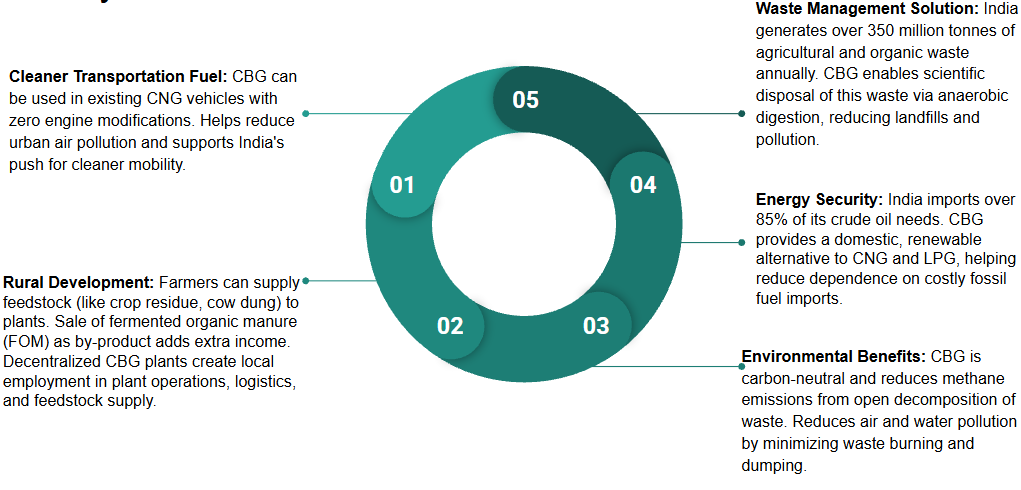

Why India Needs CBG

Market Size & Growth Potential of CBG in India

Major Players & Partnerships in India’s CBG Sector

| Category | Company | Details |

|---|---|---|

| Oil Marketing Companies (OMCs) | IOCL | 22 SATAT plants (FY23), “IndiGreen” outlets, JVs with EverEnviro & GPS |

| BPCL | CBG plant in Kochi, multiple LOIs issued for new plants | |

| HPCL | LOIs for ~100 plants (~635 TPD), actively seeking EOIs | |

| Public Sector & Energy Majors | GAIL | JV with TruAlt Bioenergy for 10 plants, ~33 million kg output |

| ONGC | JV with EverEnviro for 10 plants; 0.75 million t CO₂ savings expected | |

| Mahanagar Gas Ltd (MGL) | 2 municipal-waste plants (Deonar), 1,000 TPD, ₹600 crore investment | |

| Private & Clean Energy Firms | EverEnviro | ~20 plants across MP, UP, Delhi, Punjab; partners: IOCL, IGL, ONGC |

| GPS Renewables | JV with IOCL; setting up multiple CBG projects | |

| Adani TotalEnergies | Plans to set up 5 CBG plants under SATAT | |

| Reliance Industries | Targeting 100 CBG plants under SATAT | |

| Technology & EPC Providers | Biofics, Hycons, MOJJ | Design & build modular CBG systems with proprietary tech |

| SPS Bio-Chem, Vedavya | Provide purification and turnkey EPC solutions for CBG plants |

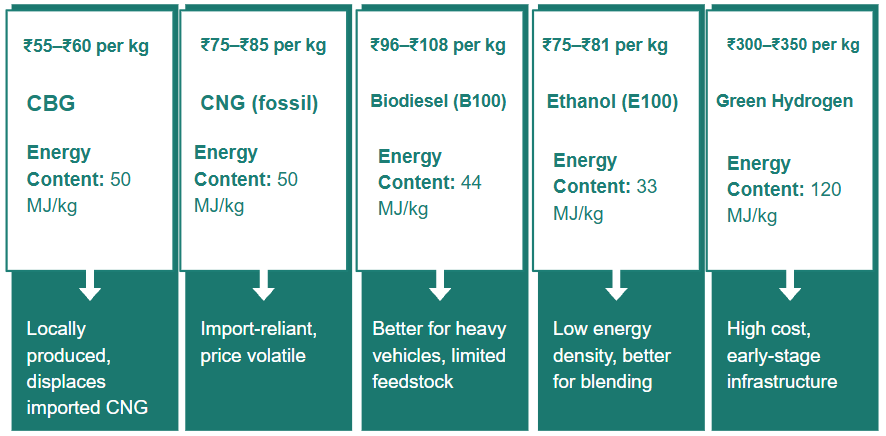

Cost Comparison of Sustainable Fuels in India

Financials and ROI

| Parameter | Details |

|---|---|

| Plant Capacity | 2–10+ TPD (Tonne Per Day) |

| CapEx (Setup Cost) |

|

| CapEx Components |

|

| Annual Operating Cost (OpEx) | ₹20–30 lakh per TPD capacity |

| Revenue Streams |

|

| Example: 5 TPD Plant |

|

| Returns |

|

| Factors Improving ROI |

|

| Government Support |

|

Challenges & Mitigation – Supply, Cost, Market Access, and Slurry Management

| Category | Challenge | Mitigation Strategy |

|---|---|---|

| 1. Feedstock Supply | – Seasonal availability of agri residue and cattle dung – Logistics cost for collecting dispersed biomass |

– Cluster-based approach: Set up plants near feedstock hubs (e.g., dairy clusters, mandis, urban waste centers) – Feedstock aggregation via FPOs, SHGs, cooperatives – Contract farming or tie-ups with farmers & gaushalas |

| 2. High CapEx & Financing Hurdles | – Setup cost is high (₹2–3 crore per TPD) – Limited access to low-cost capital, especially for MSMEs |

– Subsidies & grants via GOBARdhan, MNRE, SATAT – Priority lending by NABARD, SIDBI, IREDA with extended repayment terms – Viability gap funding for rural/small plants |

| 3. Market Access for CBG | – Limited CBG filling stations – Lack of infrastructure for grid/pipeline connectivity |

– More LOIs from OMCs under SATAT with location planning – Promote decentralized use (e.g., buses, industries, microgrids) – Set up buffer storage hubs and private dispensing points |

| 4. Digestate/Fertilizer Management | – Low awareness about bio-slurry benefits – Difficulty in transporting or monetizing slurry |

– Convert slurry into branded organic fertilizers – Partner with fertilizer firms for co-marketing – Educate farmers and demo plots to show field benefits |

Challenges & Mitigation – Technology, Policy, Skills, and Awareness

| Category | Challenge | Mitigation Strategy |

|---|---|---|

| 1. Technology Standardization | – Inconsistent digester performance – Lack of standard protocols for purification/compression |

– Promote BIS standards for CBG quality, design – Encourage validation via MNRE/test labs – Support innovation via startup grants |

| 2. Policy & Regulatory Bottlenecks | – Multiple departments (MNRE, MoPNG, MoEFCC) involved – Delays in land, environmental clearance |

– Single-window clearance for bioenergy – Declare CBG a priority infra sector – States to set up dedicated bioenergy facilitation cells |

| 3. Skilled Manpower Shortage | – Lack of trained personnel in operations, QC, maintenance | – CBG training under Skill India/PMKVY – Public-private tie-ups with ITIs/engineering colleges – Hands-on modules at demo plants |

| 4. Public Awareness | – Lack of knowledge among farmers, industries, public | – Awareness campaigns via KVKs, fairs, demo plants – Promote CBG through “IndiGreen” branding – Share farmer success stories |

India’s Competitive Advantages in CBG Manufacturing

| Advantage Area | Why India Has an Edge |

|---|---|

| 1. Abundant Feedstock | India generates over 730 million tonnes of agricultural residue and 150+ million cattle produce dung, plus 60–65 million tonnes of urban organic waste annually. This makes India one of the richest bio-waste resource nations globally. |

| 2. Large Domestic Market | Over 5,500 CNG stations and a growing fleet of CNG/CBG vehicles. India has one of the world’s fastest-growing demand for alternative transport fuels. |

| 3. Government Push | Robust policies like SATAT, GOBARdhan, MNRE Bio-Energy Programme, and PLI schemes. Guaranteed offtake of CBG by OMCs (IOCL, BPCL, HPCL) provides price certainty. |

| 4. Cost Advantage | Lower setup and labor costs compared to Europe or North America. Indigenous EPC companies (e.g., GPS Renewables, Biofics) offer low-cost modular plant designs. |

| 5. Rural Development Focus | CBG directly supports rural job creation, fits into India’s farm-waste management, and aligns with “Doubling Farmers’ Income” and Atmanirbhar Bharat missions. |

| 6. Policy-Backed Demand | India’s import dependence on energy (~85% of oil & 50% of natural gas) makes CBG a strategic fuel. Replacing imported LNG/CNG with domestic CBG reduces the forex burden. |

| 7. Growing Tech Ecosystem | India’s growing climate-tech startup ecosystem and low-cost engineering talent provide an edge in innovative purification, gas upgrading & automation. |

| 8. Public-Private Synergy | India has strong collaboration between public sector (OMCs, municipalities) and private firms (Adani, Reliance, EverEnviro) for rapid scaling. |

Government Support & Policies for CBG in India

| Policy / Scheme | Ministry / Authority | Key Features | Impact on CBG Manufacturing |

|---|---|---|---|

| SATAT (2018) Sustainable Alternative Towards Affordable Transportation |

Ministry of Petroleum & Natural Gas (MoPNG) | – Targets 5,000+ CBG plants producing 15 MTPA – OMCs (IOCL, BPCL, HPCL) to buy CBG via guaranteed offtake LOIs – Minimum price assurance for CBG |

Encourages private investment with demand security. Provides long-term revenue stability |

| GOBARdhan Scheme (Galvanizing Organic Bio-Agro Resources Dhan) |

Ministry of Jal Shakti Ministry of Rural Development |

– Funds biogas/CBG plants in villages and ULBs – Financial assistance for setting up plants using cattle dung, agri waste – Convergence with Swachh Bharat, Smart Cities |

Promotes decentralized rural CBG plants. Enhances waste collection and feedstock security |

| MNRE Bio-Energy Programme (2021–26) | Ministry of New & Renewable Energy (MNRE) | – Provides capital subsidies up to ₹50 lakh/MW equivalent – Technical support and standardization of plants – Focus on innovative technology deployment |

Reduces CapEx burden. Promotes tech innovation in biogas manufacturing |

| Waste to Energy Programme | MNRE (with MoEFCC support) | – Incentivizes municipal and industrial waste-based biogas plants – Priority to urban organic waste-to-CBG projects – Helps with environmental clearance and land |

Integrates CBG with solid waste management missions |

| PLI for Green Energy / Bioenergy (upcoming) | MNRE / NITI Aayog (in consultation) | – Potential Production Linked Incentive (PLI) under design for green fuels, including biogas – Expected to support scale manufacturing of digesters, compressors, purification units |

Will boost domestic manufacturing of CBG plant equipment |

| Priority Sector Lending (PSL) | RBI, SIDBI, NABARD | – CBG projects qualify under priority sector for green loans – Banks, NBFCs offer low interest & longer tenure loans |

Improves access to low-cost finance, especially for MSMEs |

| State-Level Subsidies | States like Haryana, Punjab, Maharashtra, MP, UP, etc. | – Land lease support, feedstock procurement aid – State EV & bioenergy policies often include CBG targets – Single-window clearances in some states |

Creates region-specific incentives and faster project clearance |

Successful CBG Projects in India

| Project / Company | Location | Capacity / Scale | Feedstock | Key Partners / Buyers | Financials (CapEx / IRR / Payback) | Impact |

|---|---|---|---|---|---|---|

| EverEnviro | MP, Delhi, UP, Punjab | 20+ plants (~80–100 TPD total) | Municipal waste, agri waste, cow dung | IOCL, IGL, ONGC | ₹10–12 Cr per plant (5–10 TPD) IRR: 16–18% Payback: 4–5 years |

300+ jobs created, 25–30% CNG replacement in local clusters |

| GPS Renewables | Karnataka, Maharashtra | Modular 2–5 TPD plants | Kitchen & agri waste | IOCL, industrial kitchens | ₹4–8 Cr per plant IRR: 14–20% Payback: ~4 years |

Automated operations, branded organic fertilizer sales |

| Adani TotalEnergies (Planned) | Gujarat, Haryana, Maharashtra | 5 large-scale plants (10–15 TPD each) | Press mud, dairy waste, paddy straw | HPCL, internal group units | ₹20–25 Cr per plant IRR: 18–22% (estimated) |

Feedstock sourced internally; strong infra and logistics |

| Mahindra Group (Pilot) | Pune, Maharashtra | Small demo plant | Canteen & garden waste | Internal use | Low CapEx due to captive waste Payback: ~3 years |

Reduced LPG/CNG costs at R&D facilities |

| MGL Deonar Project (Upcoming) | Mumbai, Maharashtra | 1,000 TPD waste processed ~70,000 kg CBG/day | Municipal organic waste | BMC, MGL, BEST buses | ₹600 Cr project cost IRR: 15–18% (expected) |

Will fuel 2,000+ buses, 400+ direct jobs |

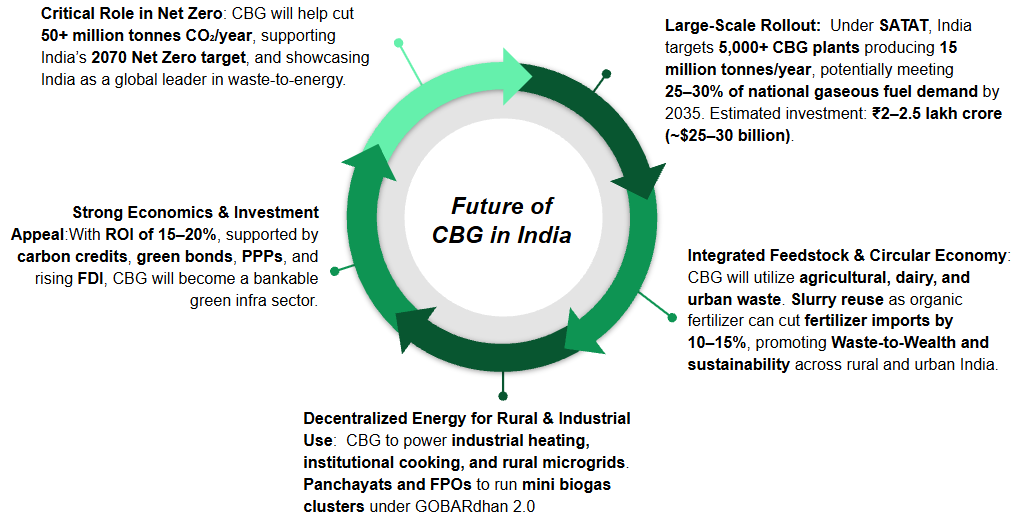

MOVING FORWARD

Massive Market Opportunity: With <1% of the 5,000 SATAT target met, there’s huge scope to grow — but only invest where you can secure land, permits, and local community support quickly.

Abundant Feedstock Availability: India has 730 Mt agri waste, 150+ million cattle, and 60+ Mt urban waste — invest near stable feedstock sources (dairy clusters, sugar mills, cities) with year-round supply contracts.

Policy Backing & Assured Demand: SATAT LOIs, GOBARdhan, and MNRE subsidies ensure stable pricing and offtake — ensure you get a firm offtake LOI from an OMC or large industrial buyer before committing capital.

Strong Return Potential: ₹2–3 crore/TPD investment can yield 14–20% IRR with 4–6 year payback — only achievable if plant uptime is 85–90% and digestate is also monetized efficiently.

Growing CNG/CBG Demand: Over 5,000 CNG stations and rising demand in transport/fleet sector — choose plant locations near demand clusters to reduce transport and boost offtake.

Green & ESG-Aligned Business: Qualifies for carbon credits and boosts sustainability credentials — register for carbon credit programs early and track methane capture and slurry usage for impact reporting.

Private & FDI Interest Rising: Giants like Adani, Reliance, IOCL are already entering — early-movers with solid project execution and scale can attract follow-on funding or M&A exits.

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in