Strategic Insights Report: Bioplastics

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

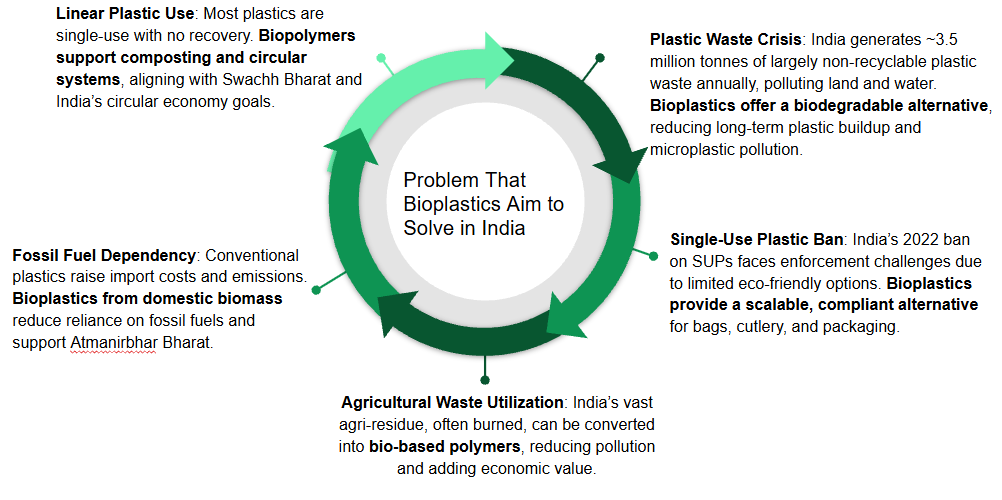

Introduction

Bioplastics are a category of plastics that are either bio-based (made from renewable resources like corn starch, sugarcane, or cellulose) or biodegradable (able to break down naturally through microbial action), or both. They offer an eco-friendly alternative to conventional petroleum-based plastics, which are a major source of long-lasting pollution.

Biopolymers, on the other hand, are naturally occurring polymers or those synthesized from biological sources. These include materials like PLA (Polylactic Acid), PHA (Polyhydroxyalkanoates), starch blends, and cellulose derivatives. Unlike traditional plastics, many biopolymers are designed to degrade under specific conditions, reducing their environmental footprint.

With increasing global concern over plastic pollution, climate change, and fossil fuel dependency, bioplastics and biopolymers are emerging as a critical part of the circular economy, especially in packaging, agriculture, medical, and automotive applications. Their development supports global sustainability goals by reducing greenhouse gas emissions, lowering dependency on crude oil, and minimizing non-degradable waste.

Market Size For Bioplastics in India

- Current Market Size (as of 2024–25)

- India’s bioplastics market is currently valued at approximately ₹3,000–3,500 crore (~$400–450 million).

- Domestic production capacity is estimated at 25,000–30,000 tonnes per annum (TPA).

- Most bioplastics used in India are imported, particularly PLA, PBAT, and PHA, due to limited local manufacturing.

- Growth Rate & Future Projections

- The Indian bioplastics market is expected to grow at a CAGR of 20–25% over the next decade.

- By 2035, the market is projected to reach:

₹25,000–30,000 crore ($3–3.6 billion)

500,000–600,000 TPA of annual production and consumption capacity

Competitive Landscape of Bioplastics in India

| Sl No. | Company | Ownership & Primary Focus | FY / CY Latest Revenue |

|---|---|---|---|

| 1 | Lucro Plastecycle (Mumbai) | Indian SME – recycled & partially bio‑based films | FY 2023‑24: ₹ 88.9 crore |

| 2 | EnviGreen Biotech (Bengaluru) | Starch‑based compostable carrier bags & films | FY 2023 est.: ₹ 25 – 30 crore |

| 3 | Ecolastic Products (Hyderabad/Bengaluru) | Starch + veg‑oil compostable bags & packaging | FY 2022‑23 filing range: ₹ 10 – 25 crore |

| 4 | TGP Bioplastics (Indore/Satara) | Proprietary biodegradable polymer blend pellets | FY 2022‑23: “micro‑enterprise; < ₹ 5 crore” |

| 5 | Green Dot Bioplastics (US) | Specialty compostable resin importer | CY 2024 est.: US $ 3.5 M → ₹ 29 crore |

| 6 | NatureWorks LLC (US) | Ingeo™ PLA resin; setting up 75 kTPA Thai plant | CY 2024 est.: US $ 35 M → ₹ 291 crore |

| 7 | Total Corbion PLA (JV) | 100 kTPA PLA plant, Thailand; imports to India | CY 2024 Net Sales: € 133.6 M → ₹ 1,202 crore |

| 8 | Biome Bioplastics (UK) | Compostable resins for coffee pods, films, mesh | FY 2023 division revenue: £ 6 M → ₹ 63 crore |

Technical & Infrastructure Challenges

| Challenge | Why It’s a Barrier | Mitigation Strategy |

|---|---|---|

| High Production Cost | Bioplastics/biopolymers cost ≈ 2–3× more than fossil-plastics due to imported resins and low volumes. |

|

| Limited Domestic Resin Supply | India imports key biopolymer resins, raising cost and exposure to supply chain risks. |

|

| Scarce Composting & Segregation Infrastructure | Without composting systems, bioplastics behave like regular waste and won’t degrade properly. |

|

| Certification Bottlenecks | Costly and slow CPCB/BIS certification limits new entrants; greenwashing damages market trust. |

|

| Feedstock Logistics & Seasonality | Sourcing agri-waste is inconsistent and affected by regional crop patterns and stubble burning. |

|

| Technical Skill Gaps | Biopolymer production and processing require specialized training and tools. |

|

Market & Consumer Challenges

| Challenge | Why It’s a Barrier | Mitigation Strategy |

|---|---|---|

| Low Consumer & Industry Awareness | Limited understanding of benefits and use cases restricts adoption and demand. | • National awareness campaigns via CII/FICCI. • QR code-based compostability labels. • Highlight government and corporate success stories. |

| Price-Sensitive Retail Market | Higher prices deter buyers in cost-sensitive B2C markets. | • Target B2B/exports first (QSRs, FMCG, airlines). • Offer GST rebates for certified compostables. • Enable carbon credit mechanisms to reduce net costs. |

| Lack of Incentives for Brand Adoption | Many brands hesitate to switch due to cost and lack of direct consumer demand or regulatory pressure. | • Offer ESG-linked tax rebates and branding benefits for companies using bioplastics. • Mandate biopolymer usage quotas in key sectors (e.g., packaging, e-commerce, hospitality). |

| Unclear End-of-Life Path for Consumers | Consumers are often unaware of how to dispose of bioplastics properly (e.g., compost vs landfill). | • Launch public education drives on disposal methods. • Mandate clear labeling (e.g., “Industrial Compost Only” or “Home Compostable”). • Integrate QR-code based instructions and incentives for proper disposal. |

Financial Viability of a Minimum Viable Bioplastics Plant (MVP)

Key Financial Metrics – MVP

-

- IRR: 18%–20%

- Payback Period: 4.5–5 years

- Net Profit Margin: 12%–15%

- Breakeven Units: ~625 TPA

| Parameter | Value |

|---|---|

| Capacity | 1,000 TPA |

| Product | PLA / Starch-based Bioplastics |

| Total Capex | ₹11 Cr |

| Annual Revenue | ₹18 Cr |

| Operating Cost | ₹11.5 Cr |

| EBITDA | ₹6.5 Cr (~36% Margin) |

Impact of Economies of Scale on ROI & Payback

| Capacity (TPA) | Capex (₹ Cr) | Capex/TPA (₹L/T) | Opex/TPA (₹L/T) | IRR | Payback |

|---|---|---|---|---|---|

| 1,000 | ₹11 Cr | ₹1.10 | ₹11.5 | 18–20% | 4.5–5 yrs |

| 5,000 | ₹32 Cr | ₹0.64 | ₹8.5 | 24–26% | 3.5–4 yrs |

| 10,000 | ₹75 Cr | ₹0.75 | ₹6.5 | 28–32% | 3.0–3.5 yrs |

| 20,000 | ₹130 Cr | ₹0.65 | ₹5.5 | 30–34% | 2.5–3 yrs |

10-Year Growth Outlook: Bioplastics in India

- eco-conscious consumer demand.

- Production Expansion: Bioplastics capacity to grow from ~30,000 to 500,000+ tonnes/year by 2035.

- Policy Support: Strong backing from SUP bans, Startup India, CPCB/BIS certifications, and green procurement norms.

- Export Opportunity: India to emerge as a key exporter of cost-effective, certified bioplastics to EU, Asia-Pacific, and Middle East.

- Investment Potential: ₹8,000–10,000 crore ($1–1.2B) projected in new bioplastic plants and R&D.

- Circular Economy Impact: Integral to India’s Net Zero 2070 and Swachh Bharat missions.

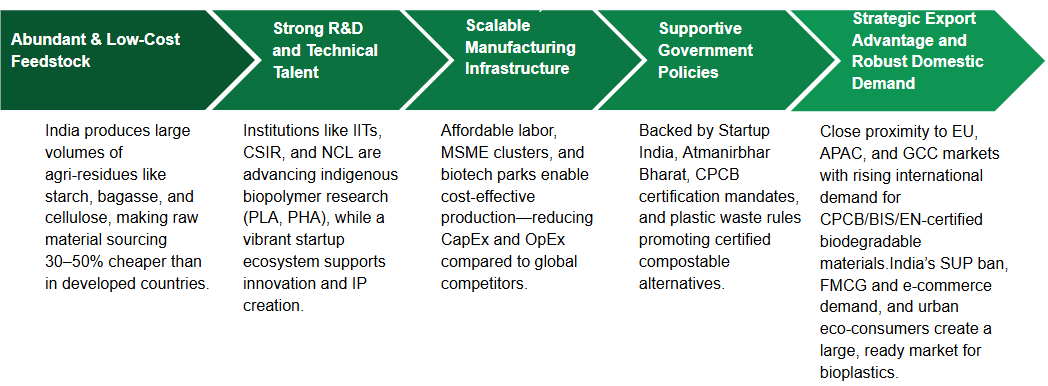

India’s Strategic Advantages in Bioplastics Manufacturing

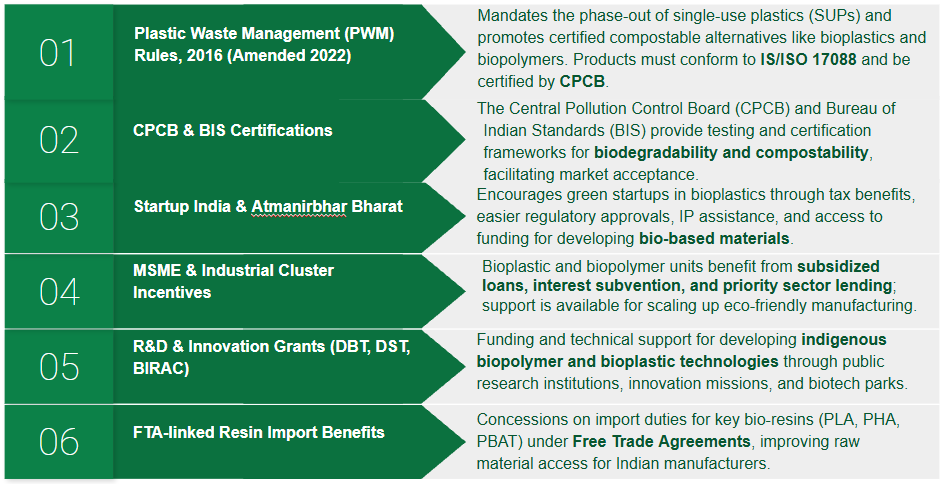

Government Support & Policies for Bioplastics

Successful Case Studies of Bioplastics Adoption in India

- Ecolastic (Hyderabad): Supplies certified compostable bags and liners to 150+ retailers and institutions; rapidly scaled post-SUP ban.

- Envigreen Biotech (Bengaluru): Produces starch-based, water-soluble bags; adopted by Bengaluru Municipal Corporation for public waste management.

- Truegreen (Mumbai): Supplies PLA/PBAT bioplastics to BigBasket, Swiggy, Zomato, and Amazon; manufactures 3,000+ tonnes/year with TÜV certification.

- TGP Bioplastics (Maharashtra): Developed low-cost CPCB-certified biodegradable bags (< ₹3/bag) for MSMEs; featured in Startup India Showcase.

- IRCTC & Indian Railways: Piloted bioplastic packaging in catering operations to reduce plastic waste in trains and stations.

- Tata Chemicals (Mithapur): Developing scalable biopolymers from marine biomass and starch for industrial packaging; export-oriented pilot underway.

MOVING FORWARD

Why Invest Now:

- Exploding Market Demand: India’s ban on single-use plastics and global sustainability mandates are creating strong B2B and B2C demand for biodegradable alternatives.

- Raw Material Advantage: Abundant, low-cost agri-waste and marine biomass make India a feedstock-rich and cost-competitive manufacturing hub.

- Policy & Regulatory Push: Supportive government schemes (PWM Rules, Startup India, MSME incentives, CPCB certification pathways) are creating a pro-investment environment.

- Diverse End-Use Sectors: Demand spans packaging, medical, agriculture, textiles, and even 3D printing, ensuring multi-sector revenue potential.

- Export Potential: India is well-placed to serve cost-sensitive, regulation-driven global markets (EU, Japan, Southeast Asia) with CPCB/EN-certified bioproducts.

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in