Strategic Insights Report: Battery Cell Manufacturing

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

INDEX

- Executive Summary

- India’s Strategic Battery Imperative

- Technology Landscape

- Cell Design Economics

- Market Landscape & Future Potential

- Value Chain Positioning

- Unit Economics

- Competitive Landscape

- Regulatory Tailwinds & Certifications

- Risk Analysis and Mitigation

- Call to Action

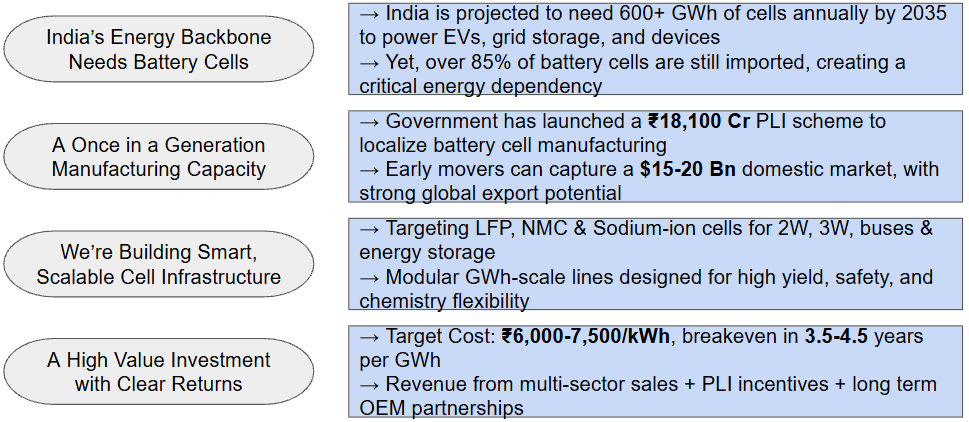

EXECUTIVE SUMMARY

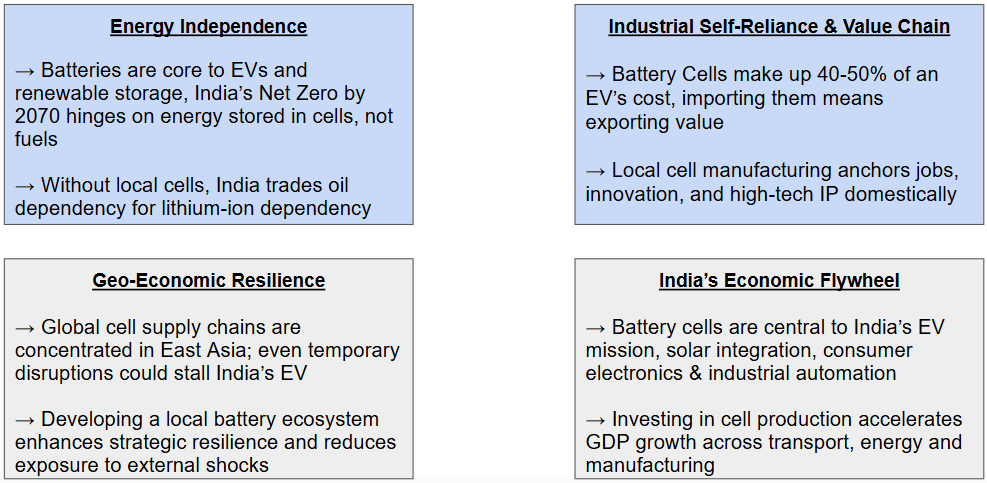

INDIA’S STRATEGIC BATTERY IMPERATIVE

TECHNOLOGY LANDSCAPE

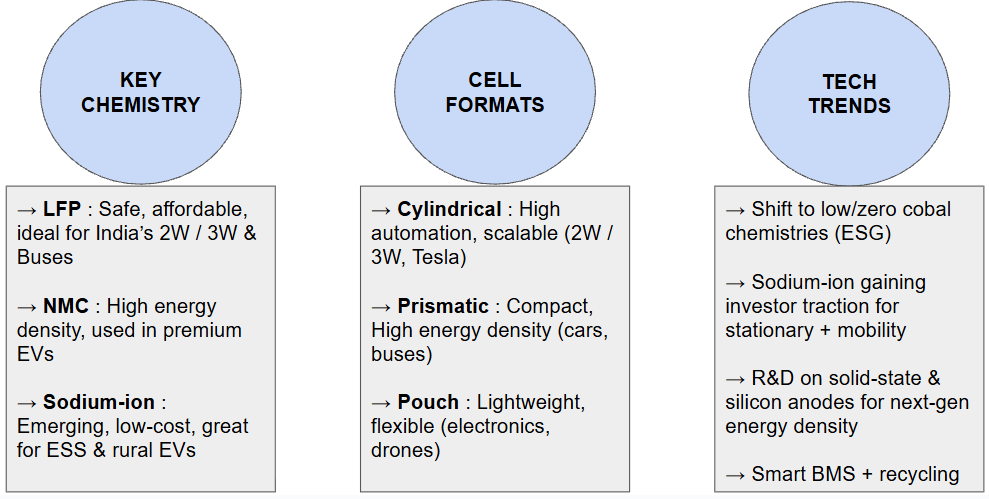

CELL CHEMISTRY LANDSCAPE

| Chemistry | Energy Density | Safety | Cost | Applications |

|---|---|---|---|---|

| LFP (LiFePO₄) | Medium (~160 Wh/kg) | Very High | Low | 2W/3W, buses, energy storage |

| NMC (811/622) | High (200–250 Wh/kg) | Medium | Medium–High | 4W EVs, premium vehicles |

| NCA | Very High | Moderate | High | Tesla/long range vehicles |

| Sodium-ion | Low–Medium | High | Very Low | Stationary storage, 2W/3W |

| Solid-State | Very High (300+ Wh/kg) | Very High | High (R&D stage) | Future EVs, drones, defense |

DESIGN FORMAT vs ECONOMICS

| Cell Format | Capex Cost (per GWh) | Energy Density | Use Case | Yield & Automation |

|---|---|---|---|---|

| Cylindrical | ₹350–400 Cr | Medium (~160–180 Wh/kg) | 2W, 3W, power tools | High yield, scalable |

| Prismatic | ₹450–500 Cr | High (~200–220 Wh/kg) | Cars, buses, ESS | Moderate complexity |

| Pouch | ₹500–550 Cr | High (~220+ Wh/kg) | Electronics, niche EVs | Low yield, higher QC need |

CELL DESIGN ECONOMICS

| Component | Share of Total Cost (%) | Estimated Cost (₹/kWh) |

|---|---|---|

| Cathode (LFP material) | ~35–40% | ₹2,400–₹3,000 |

| Anode (Graphite, Binder) | ~10–12% | ₹700–₹900 |

| Electrolyte & Separator | ~15–17% | ₹1,000–₹1,300 |

| Cell Casing + Tabs | ~8–10% | ₹600–₹750 |

| Labor, Utilities, O&M | ~8–10% | ₹600–₹750 |

| Depreciation + CapEx Recov. | ~10–12% | ₹700–₹900 |

| Total Estimated Cost | — | ₹6,500–₹7,600 per kWh |

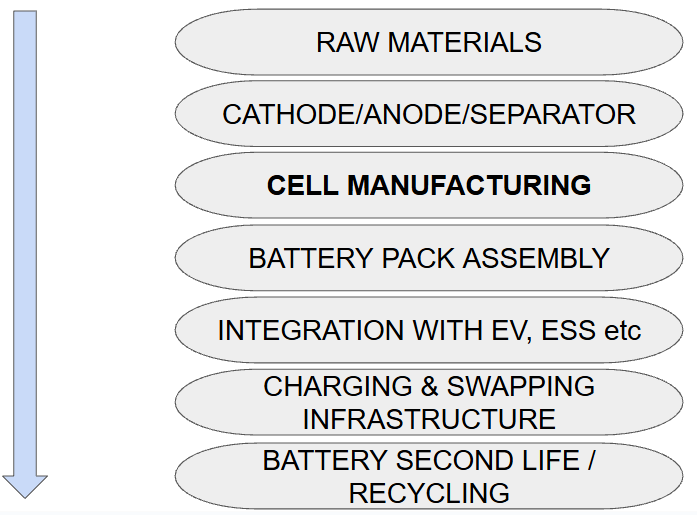

BATTERY CELL VALUE CHAIN POSITION

MARKET LANDSCAPE & POTENTIAL

- India’s current cell demand : ~12-15 GWh/year

→ Driven by 2W/3W/4W EVs, grid storage pilots, and electronics

- Domestic Cell Production : <2 GWh / year

→ Mostly pilot lines by Ola, Amara Raja, and Exide – Leclanche

- Heavy reliance on imports from China, Korea, Japan

2025 – 2035 Demand Outlook

- Total annual demand expected by 2030 : 120 -150 GWh/year

→ EVs (2W/3W/4W, buses): ~80 – 100 GWh

→ Stationary storage (grid-scale, C&I, residential): ~20 – 30 GWh

→ Consumer electronics: ~10 – 15 GWh

- By 2035: India’s total cell demand to exceed 600 GWh cumulative, with annual demand nearing 250 GWh/year

- Cell demand in India is growing at 35 – 40% CAGR through 2030

SUPPLY SIDE

| Company | Planned Capacity | Timeline | Chemistry | Notes |

|---|---|---|---|---|

| Ola Electric | 5 GWh (Phase 1) | 2025 | LFP | Targeting 100 GWh by 2030 |

| Reliance New Energy | 5 GWh (Phase 1) | 2025–26 | LFP, NMC, Sodium | Dhirubhai Ambani Giga Complex |

| Exide–Leclanché | 1.5 GWh | 2024 | LFP | Gujarat facility operational soon |

| Amara Raja Energy | 2 GWh (Phase 1) | 2025 | LFP | Telangana Giga Factory underway |

| Rajesh Exports | 5 GWh | 2025 | TBD | PLI winner |

UNIT ECONOMICS

| Component | Share of Total Cost | Estimated Cost (₹/kWh) |

|---|---|---|

| Cathode (LFP) | ~35–40% | ₹2,400–₹3,000 |

| Anode (Graphite + Binder) | ~10–12% | ₹700–₹900 |

| Electrolyte + Separator | ~15–17% | ₹1,000–₹1,300 |

| Casing, Tabs, Collector | ~8–10% | ₹600–₹750 |

| Labor + Utilities | ~8–10% | ₹600–₹750 |

| Depreciation + CapEx Load | ~10–12% | ₹700–₹900 |

| Total Cost | — | ₹6,500–₹7,600 per kWh |

COMPETITIVE LANDSCAPE

| Investor | Technology | Investment Size | Capacity | Location |

|---|---|---|---|---|

| Ola Electric | 4680 cylindrical LFP cell | $100 M (~₹825 Cr) | 5 GWh Phase‑1 → 20 GWh by 2026 | Krishnagiri, Tamil Nadu |

| Tata (Agratas Energy) | LFP cell gigafactory | ₹13,000 Cr (~$1.6 B) | 20 GWh | Sanand, Gujarat |

| Exide Energy Solutions Ltd | Advanced chemistry LFP | ₹3,600 Cr so far, +₹1,200 Cr | 6 GWh, planned expansion to 12 GWh | Bengaluru, Karnataka |

| Reliance New Energy Battery | ACC battery cells (tech‑agnostic) | Supported by ₹18,100 Cr PLI scheme | 10 GWh (PLI award) | Jamnagar, Gujarat |

| Cygni Energy | LFP cells (LEED‑certified) | ₹10 B (₹100 Cr) Phase‑1 | 4.8 GWh Phase‑1 → 10.8 GWh Phase‑2 | Maheshwaram, Telangana |

| Wardwizard Innovations | Li-ion cell assembly | ₹650 Cr | 1 GWh assembly line | Vadodara, Gujarat |

RISK ANALYSIS AND MITIGATION

| Risk Category | Description | Mitigation Strategy |

|---|---|---|

| Raw Material Volatility | Price & supply fluctuations in lithium, cobalt, nickel | Long-term contracts, recycling, local sourcing, R&D in LFP |

| Technology Obsolescence | Rapid evolution in chemistries & global innovation | Flexible manufacturing lines, partnerships, IP acquisition |

| High Capex & Long Gestation | Giga factory setup requires large upfront investment | Government PLI support, phased investment, JV models |

| Import Dependence | Reliance on imports for cell components or machinery | Develop domestic supply chain, incentives for localization |

| Regulatory Uncertainty | Policy shifts or delays in subsidy disbursal | Engage with policymakers, diversify market applications |

| Safety & ESG Concerns | Thermal runaway, emissions, labor issues in sourcing metals | Strict QA protocols, ESG-compliant sourcing, automation |

| Demand-Supply Mismatch | Oversupply risk if EV/storage adoption lags | Serve multiple segments – EVs, grid, telecom, industrial |

MOVING FORWARD

- Capitalize on the government’s ₹18,100 crore PLI scheme for Advanced Chemistry Cell (ACC) manufacturing to reduce upfront capital investment and ensure long-term financial viability.

- Form strategic R&D partnerships with global battery technology leaders to stay ahead in evolving chemistries like LFP, solid-state, and sodium-ion, ensuring future-proof product lines.

- Build secure and diversified raw material supply chains by investing in domestic mining opportunities, entering long-term offtake agreements, and exploring battery recycling as a circular solution.

- Focus on high-growth application areas such as electric two-wheelers, three-wheelers, commercial fleets, and grid-scale energy storage, where demand visibility and policy support are strong.

- Integrate strong ESG (Environmental, Social, Governance) practices from the start by sourcing ethically, minimizing emissions, and adhering to global safety standards to attract impact-focused investors.

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in

India Big Business Opportunities in Climate Tech – List – EAI

India Big Business Opportunities in Climate Tech – List – EAI