Strategic Insights Report: Data Center Decarbonization

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

INDEX

- Executive Summary

- Problem Statement

- Market Landscape

- Regulatory & Policy Drivers

- Decarbonization Strategies

- Technical Landscape

- Competitive Landscape

- Supply Chain & Infra Readiness

- Business Model

- Unit Economics

- Risk and Mitigation

- Impact Metrics

- Call to Action

ㅤ

EXECUTIVE SUMMARY

India’s data centre market is expected to grow from 870 MW (2023) to over 2,500 MW by 2027, driven by rapid digitization, AI workloads, and data localization mandates. This surge will result in a 3× increase in electricity demand, making decarbonization a strategic and regulatory priority.

ㅤ

PROBLEM STATEMENT

India’s data centre industry is expanding rapidly, projected to reach 2,500+ MW by 2027, driven by AI, cloud, and digital infrastructure growth. However, this growth is heavily carbon-intensive due to:

- Reliance on coal-dominant grid power

- Widespread use of diesel generators for backup

- Inefficient cooling systems that consume up to 50% of total energy

As a result, data centre electricity consumption is expected to rise from ~6 TWh today to ~25 TWh by 2030, making the sector a significant emitter of carbon. At the same time, investors and enterprises face growing pressure from:

- ESG mandates (SEBI’s BRSR Core, global Scope 2 targets)

- Client demand for low-carbon hosting (RE100, Net Zero commitments)

- Regulatory signals toward carbon pricing and green compliance

The Critical Challenge : How can India scale its data centre infrastructure without locking in high emissions, operational inefficiencies, and ESG compliance?

ㅤ

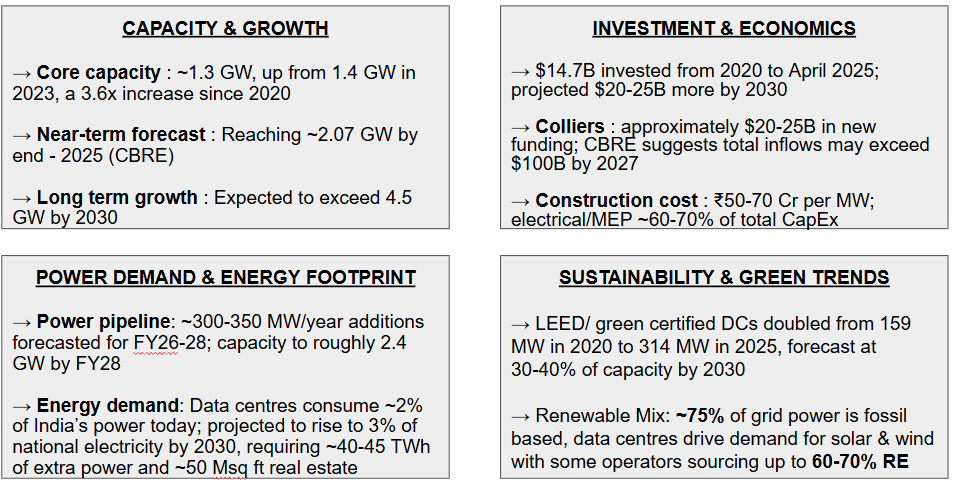

MARKET LANDSCAPE

ㅤ

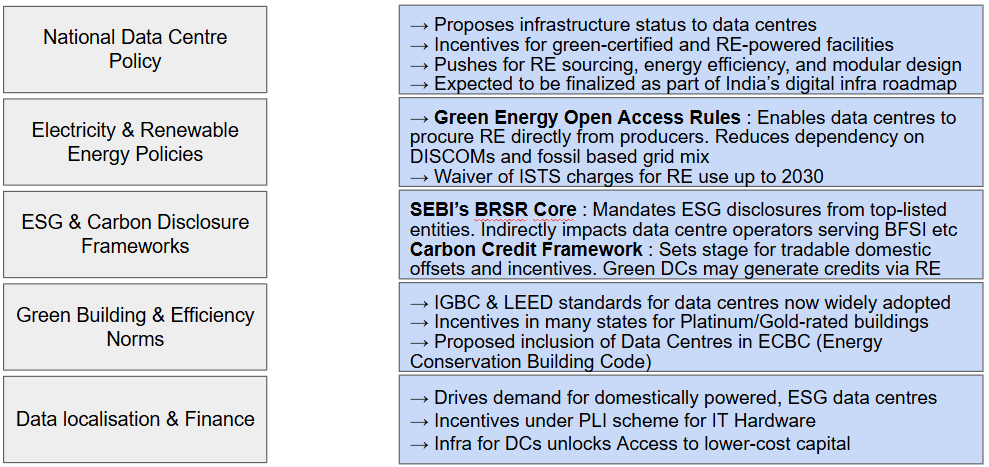

REGULATORY & POLICY DRIVERS

ㅤ

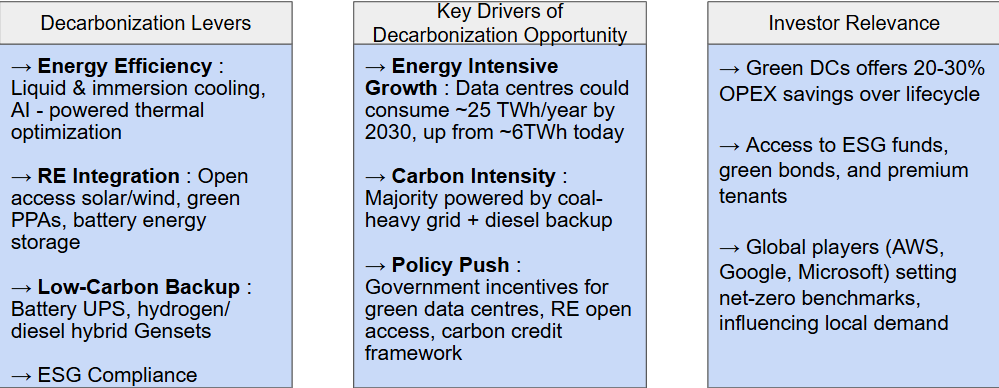

DECARBONIZATION STRATEGIES

ㅤ

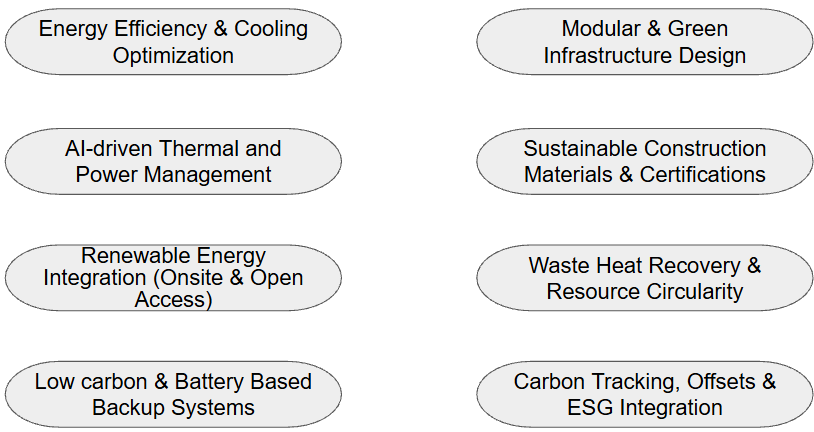

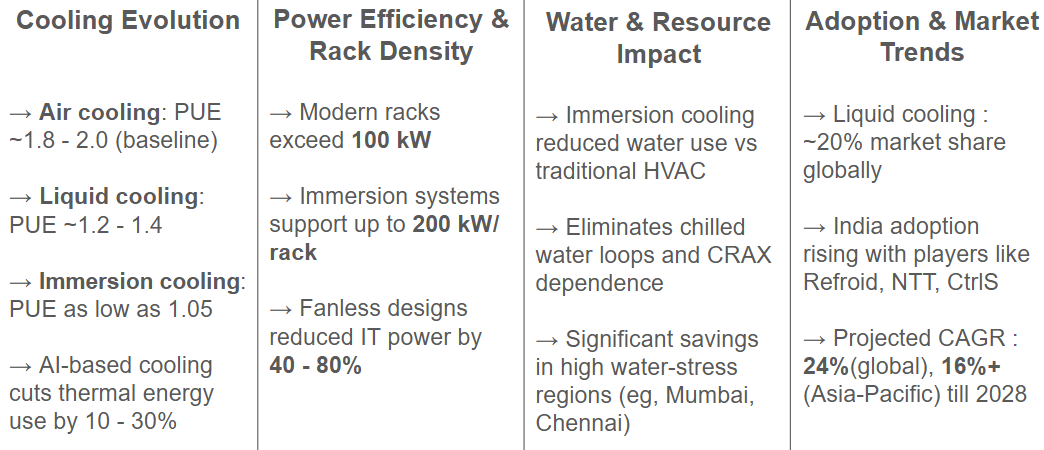

TECHNICAL LANDSCAPE

ㅤ

COMPETITIVE LANDSCAPE

Established Players (Traditional DC Giants)

| Player | Capacity (MW) | Key Decarbonization Moves |

|---|---|---|

| STT GDC | ~300+ | Green PPAs, LEED Platinum, AI cooling |

| CtrlS | ~250+ | Net Zero by 2030, solar rooftops, water reuse |

| NTT GDC | ~200+ | Captive RE plants, low-PUE cooling, BRSR reporting |

| Sify | ~100+ | Modular builds, RE sourcing in progress |

Emerging Green Players

| Player | Focus | Notable Initiatives |

|---|---|---|

| Nxtra (Airtel) | Pan-India RE-linked growth | 370 MW green PPAs signed, 60% RE share |

| AdaniConneX | Infra-scale green builds | Data centres powered by 100% RE, hydrogen trials |

| Yotta (Hiranandani) | Hyperscale + Solar | 40‑acre solar plant, immersion cooling pilots |

ㅤ

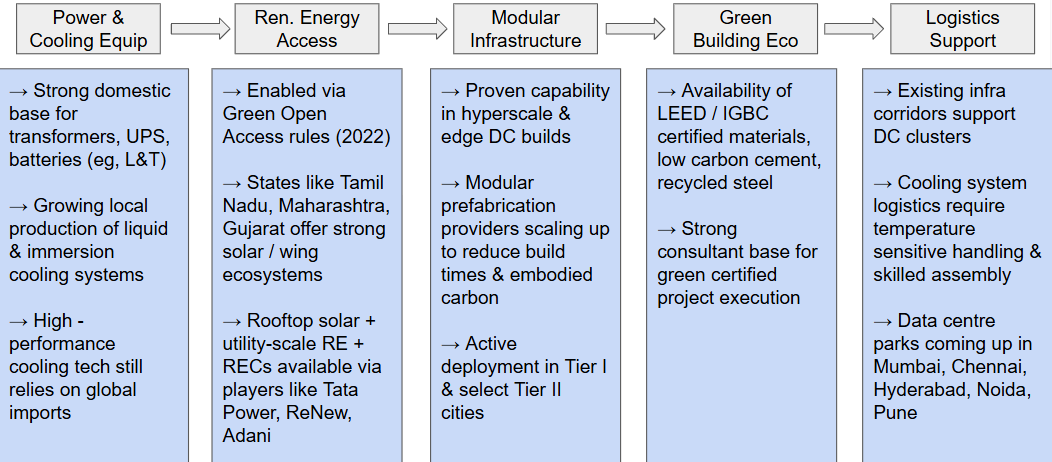

SUPPLY CHAIN & INFRA READINESS

ㅤ

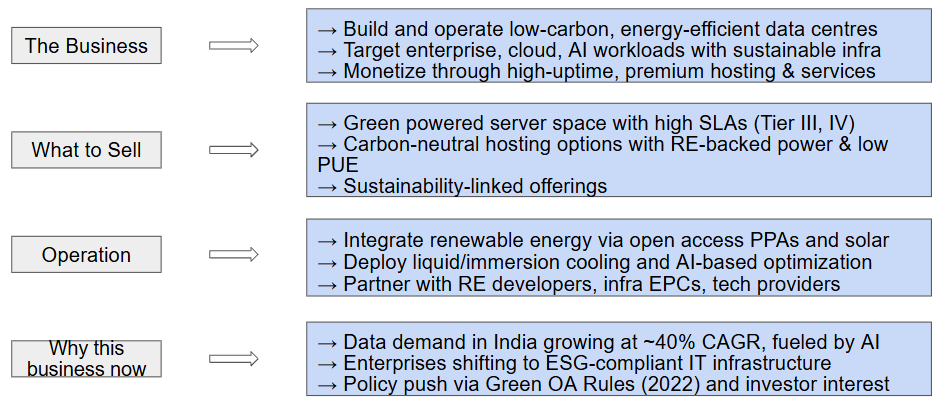

BUSINESS MODEL

ㅤ

UNIT ECONOMICS

| Parameter | Value | Remarks |

|---|---|---|

| Capex | ₹46.5 Cr (USD ~$5.4 million) | One-time infrastructure cost |

| Annual Opex | ₹44–45 Cr (USD ~$5.35 million) | Includes all recurring operational costs |

| Annual Revenue | ₹75–85 L/kW/month → ₹9–10 Cr/MW | Based on enterprise/hyperscale hosting |

| EBIT Margin | ~50–60% (post ramp-up) | High-margin model after 1–2 years |

| Payback Period | 3–5 years | Returns accelerate post stabilization |

| Decarbonization Upside | ₹40–120 L/year saved | Energy efficiency + RE sourcing benefits |

ㅤ

RECORDED INVESTMENTS

| Investor | Technology | Investment | Capacity | Location |

|---|---|---|---|---|

| Nxtra (Airtel) | Green-ready hyperscale + AI-optimized DCs | ₹5,000 Cr (~USD 600 M) | Expand from ~200 MW to 400 MW by 2027 | Pan-India (Chennai, Hyderabad, etc.) |

| Microsoft (Azure) | Self-built cloud & AI-ready data centres | USD 3 B over 2 years | Cluster capacity ~660 MW | Telangana, Pune, Mumbai, Chennai |

| AWS (Amazon Web Services) | Cloud infrastructure expansion (AI/cloud ops) | USD 12.7 B by 2030 (with ₹60 B in Maharashtra by 2029–30) | Not specified MW | India-wide; Maharashtra region highlighted |

| Adani + EdgeConneX | Green hyperscale DC development | Part of a $25 B pipeline | Target: 1 GW by 2030 | Gujarat & pan‑India |

ㅤ

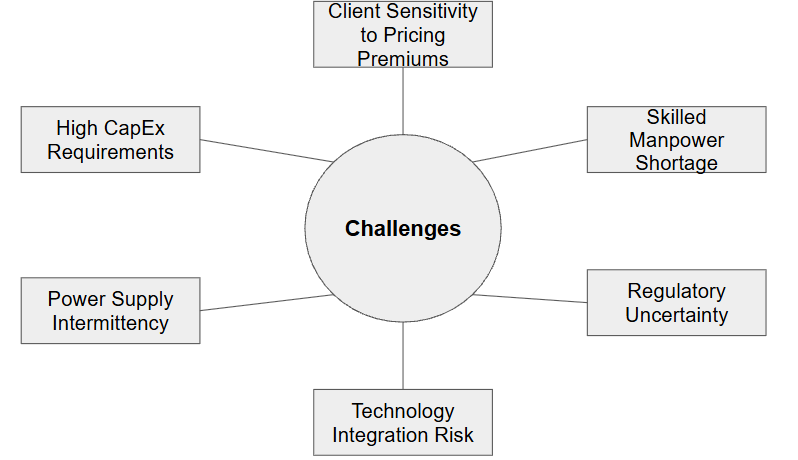

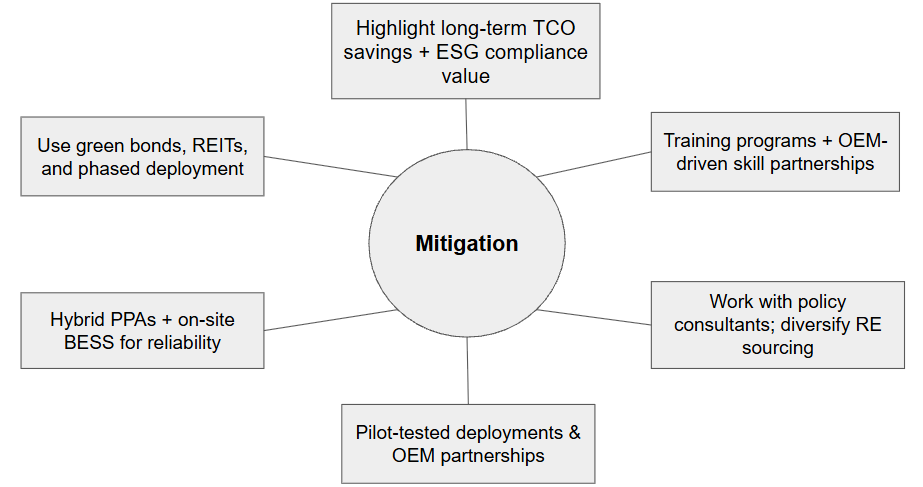

RISKS AND MITIGATION

ㅤ

SOLUTIONS

ㅤ

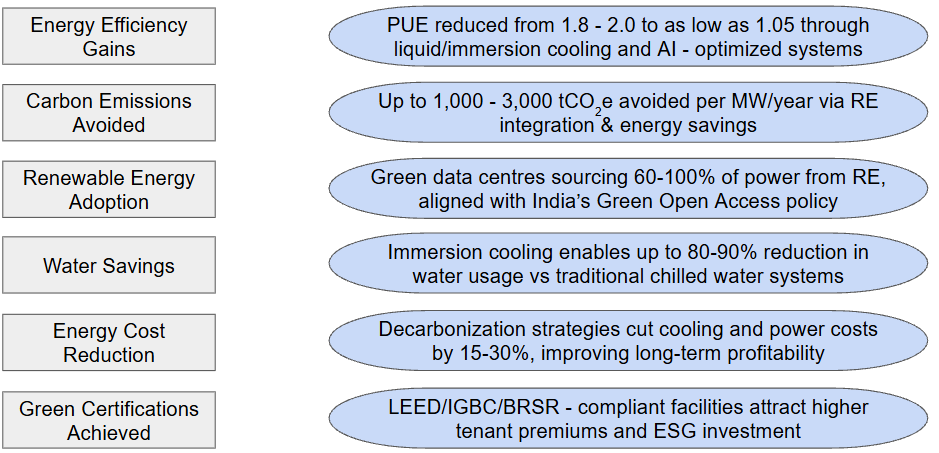

IMPACT METRICS

ㅤ

MOVING FORWARD

- Capitalize on India’s ₹1.6 trillion digital infrastructure surge by investing in data centres that are not just high-capacity, but future-proofed through sustainability, energy efficiency, and climate-aligned design.

- Invest in next-gen data centres purpose-built for AI, cloud, and hyperscale computing — all while meeting the rising global demand for ESG-compliant, net-zero digital operations.

- Unlock strong financial upside by leveraging green bonds, data centre REITs, and carbon credit revenues — turning sustainability into a core value driver, not just a compliance metric.

- Partner in developing ultra-efficient, low-PUE facilities powered by renewable energy, backed by AI-based thermal control, liquid cooling, and modular construction innovations.

- Ride the wave of favorable Indian policies like Green Open Access, RE integration mandates, and climate-linked infrastructure incentives — all creating a supportive ecosystem for green data infra.

- Enter a sector offering consistent 50–60% EBIT margins, robust tenancy contracts, and asset paybacks within 3–5 years — making it one of the most resilient and future-facing infrastructure bets today.

ㅤ

WHY PARTNER WITH EAI?

- Leading specialist in renewables, low-carbon mobility, and sustainable materials.

- Trusted advisor to Fortune 500 firms—including Reliance, World Bank, and Tamil Nadu Government.

- Deep domain expertise across bio-energy, bioplastics, biofuels via CO₃ and CLIMAFIX.

- Backed by IIT/IIM talent with strong industry, investor, and policy networks.

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in