Strategic Insights Report: Green Chemicals

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

INDEX

- Executive Summary

- Green Chemicals

- The Need & Key Drivers

- India’s Green Imperative

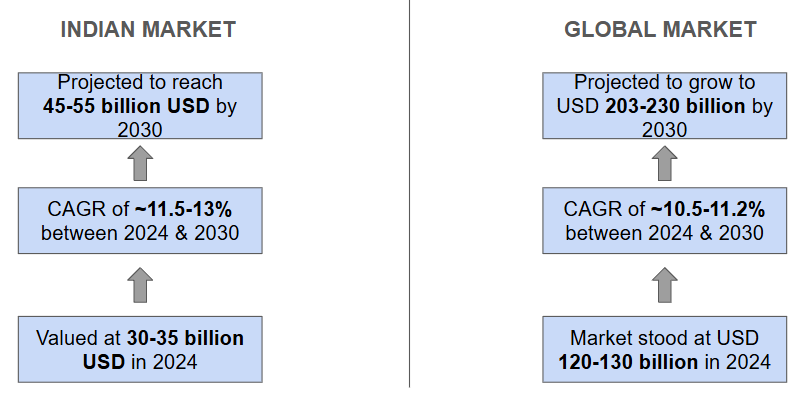

- Market Landscape & Demand Outlook

- Global Trends in Green Chemicals

- Focus Investment Segments

- Government Policies & Incentives

- Competitive & Industry Landscape

- India’s Competitive Advantage

- Financials & ROI

- Call to Action

ㅤ

EXECUTIVE SUMMARY

ㅤ

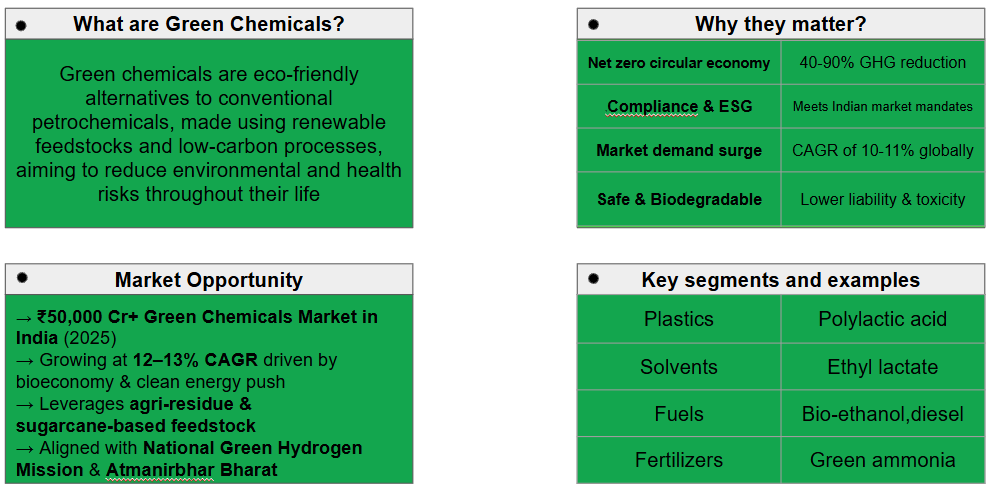

GREEN CHEMICALS

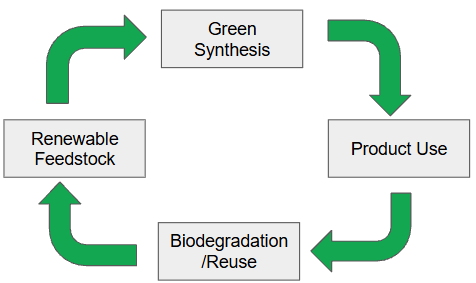

Green chemicals are substances produced through renewable, non-toxic, and low emission processes, offering sustainable alternatives to petrochemicals. In India, they help reduce imports, tap into agri-residue & support net-zero goals.

ㅤ

HOW THEY DIFFER FROM CONVENTIONAL CHEMICALS?

| FEATURE | CONVENTIONAL CHEMICALS | GREEN CHEMICALS |

|---|---|---|

| Feedstock | Fossil-based (oil, coal, gas) | Biomass, CO₂, waste |

| Process | Energy & emissions intensive | Low-carbon, enzymatic or fermentation based |

| End of life | Often toxic and non biodegradable | Biodegradable or recyclable |

ㅤ

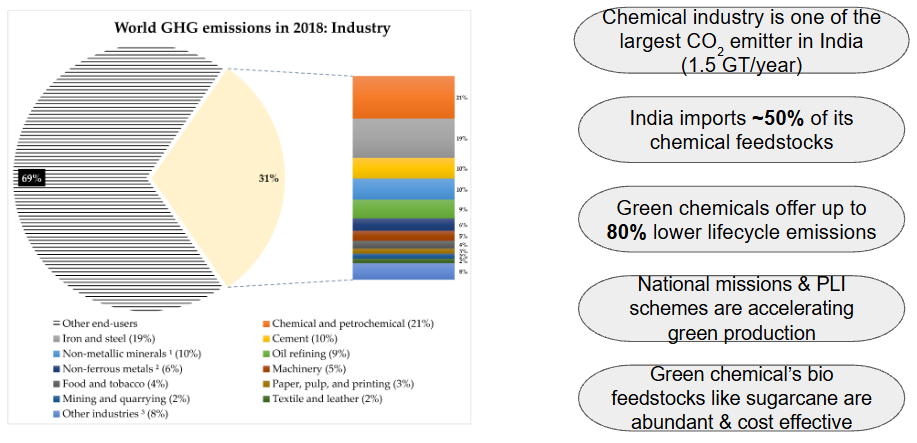

THE NEED AND KEY DRIVERS

ㅤ

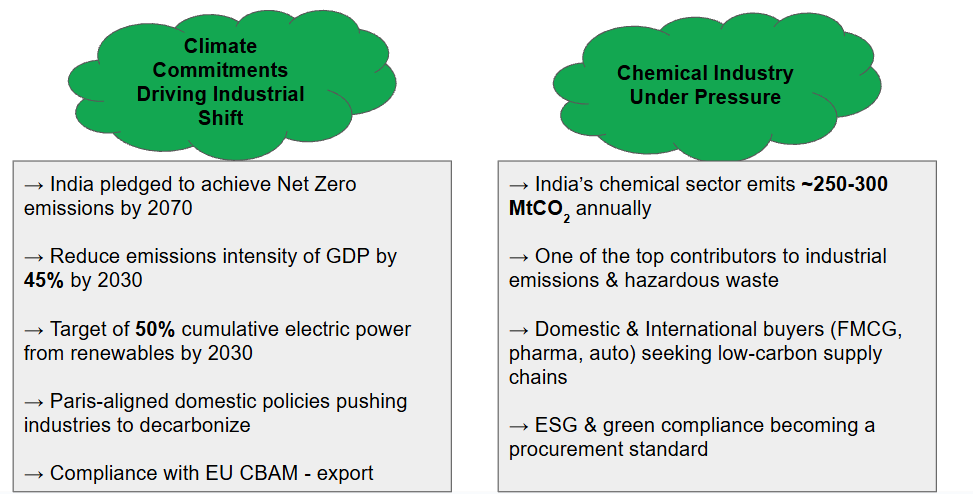

INDIA’S GREEN IMPERATIVE

ㅤ

MARKET LANDSCAPE AND DEMAND OUTLOOK

ㅤ

DEMAND DRIVERS ACROSS SECTORS

| Sector | Demand for Green Chemicals | Key Green Inputs |

|---|---|---|

| FMCG & Personal Care | High demand for natural surfactants, bioplastics, and bioethanol | Bio-surfactants, biopolymers, solvents |

| Pharma & Nutraceuticals | Rising demand for bio-based solvents, intermediates | Lactic acid, succinic acid, green solvents |

| Textiles | Eco-friendly dyes, biodegradable finishing agents | Bio-based resins, non-toxic coatings |

| Automotive | EV battery cooling, interiors, sustainable plastics | PLA, bio-PE, green composites |

| Aviation & Shipping | Decarbonization via biofuels | Green methanol, SAF intermediates |

| Agrochemicals | Push for sustainable bio-based inputs | Itaconic acid, levulinic acid, biosurfactants |

ㅤ

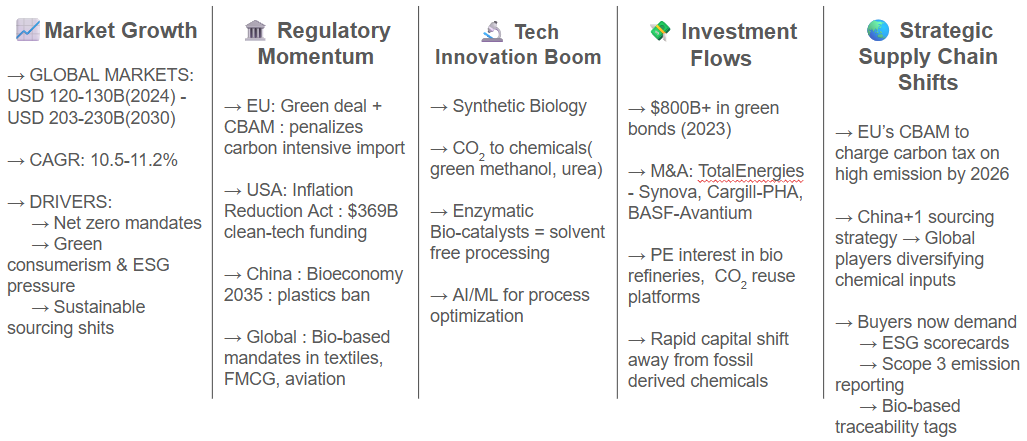

GLOBAL TRENDS IN GREEN CHEMICALS

ㅤ

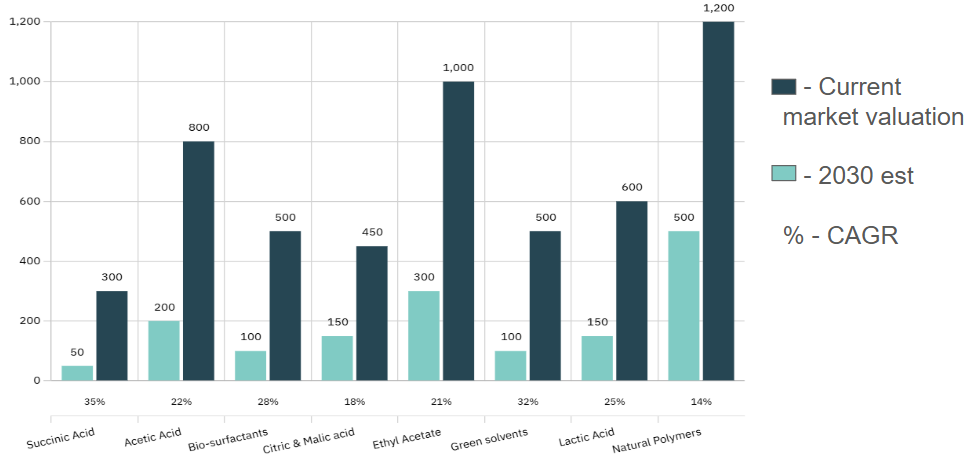

SEGMENT-WISE MARKET GROWTH ESTIMATES (Cr)

ㅤ

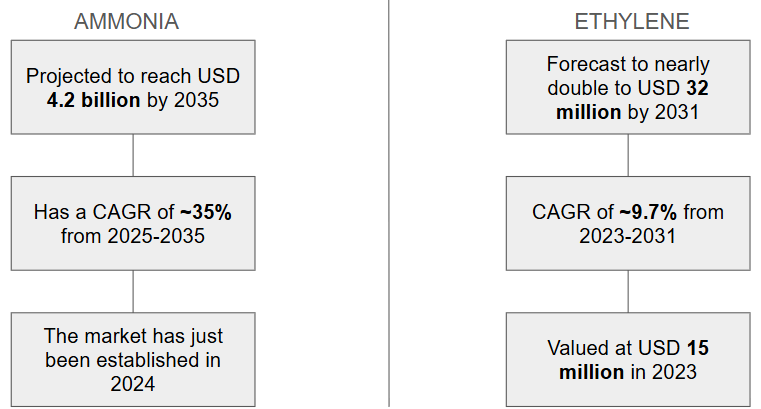

GREEN AMMONIA & ETHYLENE

Ammonia and ethylene production account for the largest share of CO₂ emissions in the chemical industry, making their transition to green alternatives critical for achieving net-zero emissions.

ㅤ

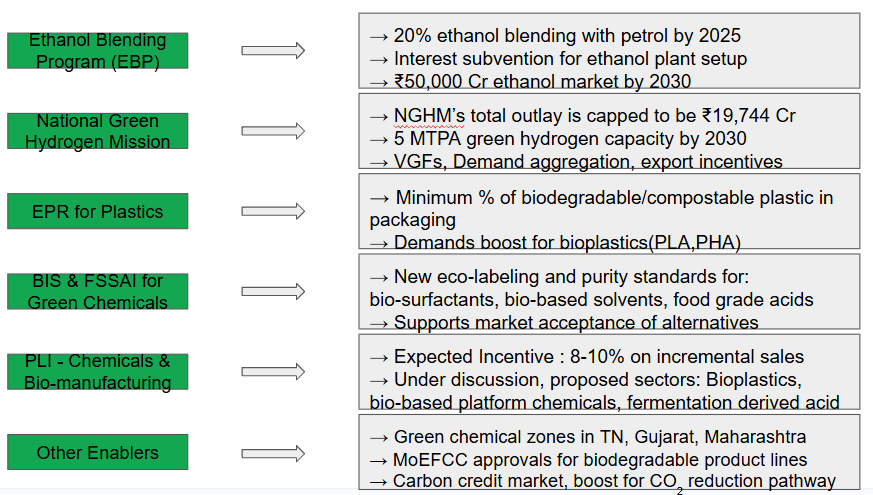

GOVERNMENT POLICIES & INCENTIVES

ㅤ

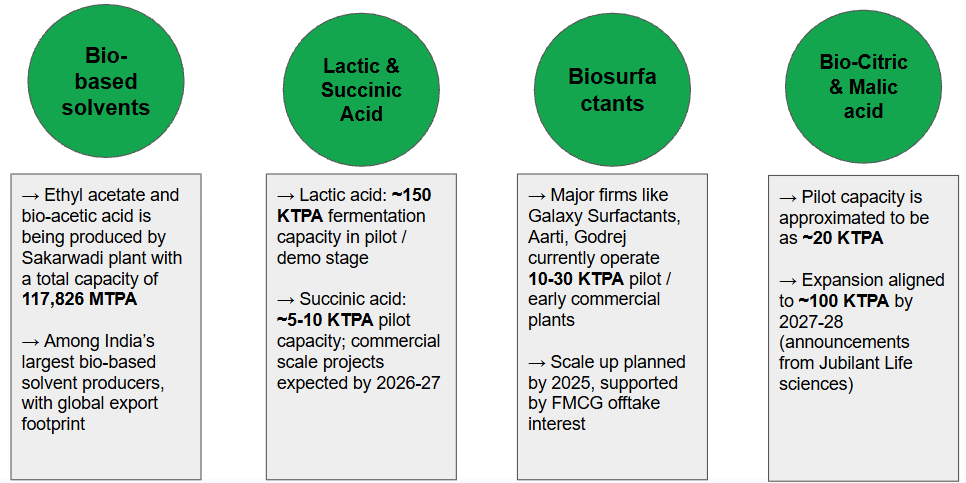

PRODUCTION AND CAPACITY

ㅤ

COMPETITIVE & INDUSTRY LANDSCAPE

| Segment | Major Indian Players | Notes |

|---|---|---|

| Lactic Acid | Godavari Biorefineries, Jubilant Life Sciences (R&D), Praj | High import dependency (~70%), domestic fermentation capacity scaling; used in food, pharma, cosmetics |

| Bio-based Acetic Acid | Jubilant Ingrevia, Godavari Biorefineries | Commercial capacity exists; used in adhesives, coatings; price-sensitive to ethanol cost vs petro variant |

| Bio-based Ethyl Acetate | Godavari Biorefineries | India’s leading bio-ethyl acetate producer; exported to EU/US; strong backward integration from molasses |

| Green Solvents (Ethyl Lactate, etc.) | Startups (under BIRAC, CSIR), Praj (pilot) | Very early-stage; small pharma/agro buyers; scope for niche applications; needs better awareness and scale-up funding |

| Bio-surfactants (Rhamnolipids, APG) | Galaxy Surfactants, Aarti Industries, Godrej | Growing demand from FMCG; current production at small-commercial scale; certification hurdles exist |

| Citric & Malic Acid (Bio-based) | Jubilant Life Sciences (proposed), Rossari Biotech (exploring) | Food/pharma/nutraceutical applications; currently 60–70% import-dependent; fermentation-based production is in early scale-up phase |

| Natural Polymers (Guar, Starch Derivatives) | Vikas WSP, Jain Chem, Universal Starch-Chem Allied | Well-established in India; used in food, oil drilling, paper; growing demand, but agri-supply volatility is a risk |

ㅤ

RECORDED GREEN CHEMICALS INVESTMENTS

| Investor | Technology | Investment Size | Capacity | Location |

|---|---|---|---|---|

| Balrampur Chini Mills | PLA biopolymer from lactic acid | ₹2850 Cr | 80,000 TPA | UP |

| Galaxy Surfactants | Bio-surfactants R&D and pilot | ₹150 Cr p.a Capex | 10–30 KTPA | Maharashtra, Gujarat |

| Godavari Biorefineries | Bio-based Acetic Acid & Ethyl Acetate | ₹130 Cr | 117826 TPA | Karnataka |

| Jubilant Life Sciences | Bio-based Citric & Malic acid | ₹250 Cr | ~20 KTPA, expansion up to 100 KTPA by 2027 | Gujarat |

ㅤ

TECHNOLOGY AND RECENT INNOVATIONS (KEY SEGMENTS)

| Pathway | Feedstock | CapEx | OpEx (₹ / kg product) | Market Price (₹/kg) | Conversion Efficiency | Tech Readiness |

|---|---|---|---|---|---|---|

| Lactic Acid (Fermentation) | Sugarcane, bagasse | ₹150–200 Cr pilot plant | ₹50–70 | ₹140–160 | ≥90% | Emerging – pilot to small |

| Succinic Acid (Metabolic) | Sugarcane/molasses | ₹200–250 Cr pilot plant | ₹80–100 | ₹250–300 | 60–70% | Pilot stage |

| Bio-Acetic Acid (Fermentation) | C5–C6 sugars | ₹300–400 Cr unit | ₹60–80 | ₹100–120 | ~85% | Semi-commercial |

| Biosurfactants (Enzymatic) | Vegetable oils, sugars | ₹150–200 Cr pilot | ₹200–250 | ₹450–550 | ~60–70% | Pilot stage |

| Ethyl Acetate | Sugarcane ethanol | ₹250–350 Cr per 100ktpa | ₹50–70 | ₹120–140 | ~80–90% | Commercial |

| Citric/Malic Acid | Molasses, corn syrup | ₹200 Cr pilot plant | ₹80–100 | ₹180–200 | ~70–80% | Pilot stage |

| Green Solvents | Agro residues, peels | ₹50–80 Cr pilot plant | ₹120–150 | ₹500–600 | ~60–70% | Early pilot |

| Natural Polymer | Guar, starch, lignin | ₹100–150 Cr plants | ₹30–50 | ₹80–120 | ~90% | Mature |

ㅤ

EXAMPLE OF GODAVARI PLANT

| Metric | Value |

|---|---|

| Annual Output | ~117,826 metric tonnes (bio-solvents combined) |

| Average Selling Price | ₹110–130 per kg (weighted avg.) |

| Gross Revenue | ₹1,300–1,500 Cr annually |

| Carbon Credit Income | ₹20–30 Cr annually |

| OPEX | ₹800–900 Cr annually |

| EBITDA | ₹400–500 Cr |

| Break-even Period | 4–5 years |

ㅤ

INDIA’S COMPETITIVE ADVANTAGE

| Advantage | Description |

|---|---|

| Feedstock abundance | Large volumes of sugarcane, rice straw, molasses, food/agri waste |

| Cost competitiveness | 30–40% lower production cost vs. EU/US |

| Policy tailwinds | EBP, SUP ban, PLI, Green Hydrogen Mission |

| Growing domestic demand | Higher ESG standards in FMCG, textiles, packaging |

| Global export potential | Cost-efficient green input hub for Asia & Africa |

ㅤ

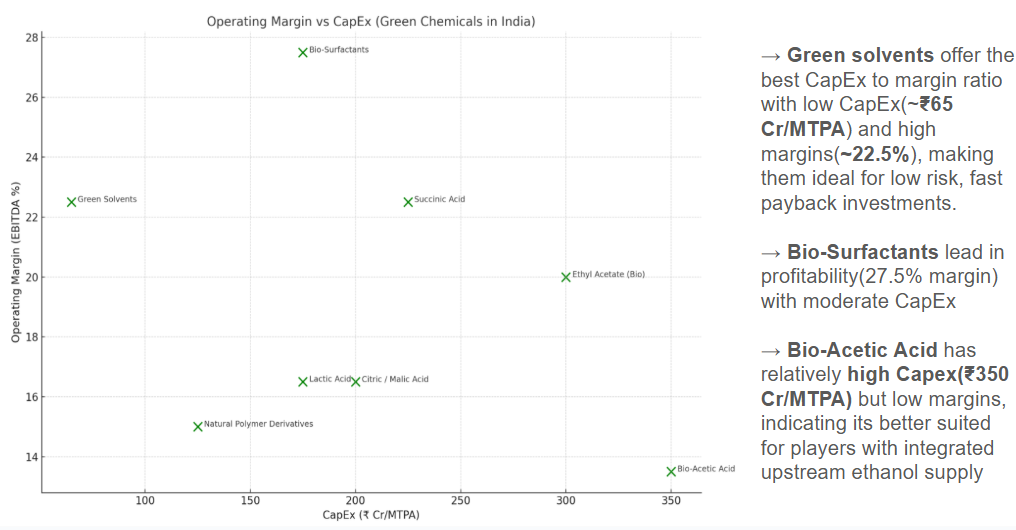

FINANCIALS & ROI

ㅤ

MOVING FORWARD

- Capitalize on a $100+ billion opportunity by investing in scalable green chemical technologies.

- Join hands with startups and research leaders to co-develop low-carbon solutions.

- Accelerate infrastructure and supply chain development through strategic funding.

- Be a proactive policy partner to shape favorable regulations and secure incentives.

- Lead the transition to circular, sustainable value chains with green alternatives.

WHY PARTNER WITH EAI?

- Leading specialist in renewables, low-carbon mobility, and sustainable materials.

- Trusted advisor to Fortune 500 firms—including Reliance, World Bank, and Tamil Nadu Government.

- Deep domain expertise across bio-energy, bioplastics, biofuels via CO₃ and CLIMAFIX.

- Backed by IIT/IIM talent with strong industry, investor, and policy networks.

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in

India Big Business Opportunities in Climate Tech – List – EAI

India Big Business Opportunities in Climate Tech – List – EAI