Why is the Indian Biofuels Market an Attractive Destination for International Investment ?

Exploring India’s Booming Biofuels Market: An Attractive Destination for International Investment

Introduction:

India’s biofuels market presents a lucrative investment opportunity for international players, driven by a combination of factors including government policies, market size projections, key players, and technological innovations. This article delves into the specifics of why the Indian biofuels market is drawing significant international interest.

The Indian biofuels market is considered an attractive destination for international investment for several reasons:

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist- Growing Energy Demand: India has a rapidly growing population and economy, leading to increased energy demand. Biofuels present a sustainable alternative to conventional fossil fuels, aligning with India’s goals to diversify its energy sources and reduce dependence on imported oil.

- Government Support: The Indian government has been actively promoting the use of biofuels through policy measures such as the National Biofuel Policy and the Ethanol Blended Petrol (EBP) Program. These initiatives provide a supportive regulatory framework and incentives for investments in biofuels production and distribution.

- Abundant Biomass Resources: India is rich in biomass resources such as agricultural residues, sugarcane bagasse, and non-edible oilseeds, which can be used as feedstock for biofuel production. This availability of raw materials ensures a stable supply chain for biofuels production.

- Environmental Benefits: Biofuels offer environmental benefits by reducing greenhouse gas emissions and air pollution compared to conventional fossil fuels. With increasing environmental concerns globally, investing in biofuels aligns with corporate sustainability goals and enhances the reputation of international investors.

- Market Potential: The Indian biofuels market has significant growth potential due to increasing consumer awareness about the environmental impact of fossil fuels, government mandates for biofuel blending, and rising demand for cleaner energy sources.

- Technological Innovation: International investors bring advanced technologies and expertise in biofuels production, which can contribute to improving efficiency, reducing production costs, and scaling up operations in the Indian market.

- Partnership Opportunities: International investors can leverage partnerships with Indian companies, research institutions, and government agencies to access local expertise, market knowledge, and resources, facilitating market entry and expansion.

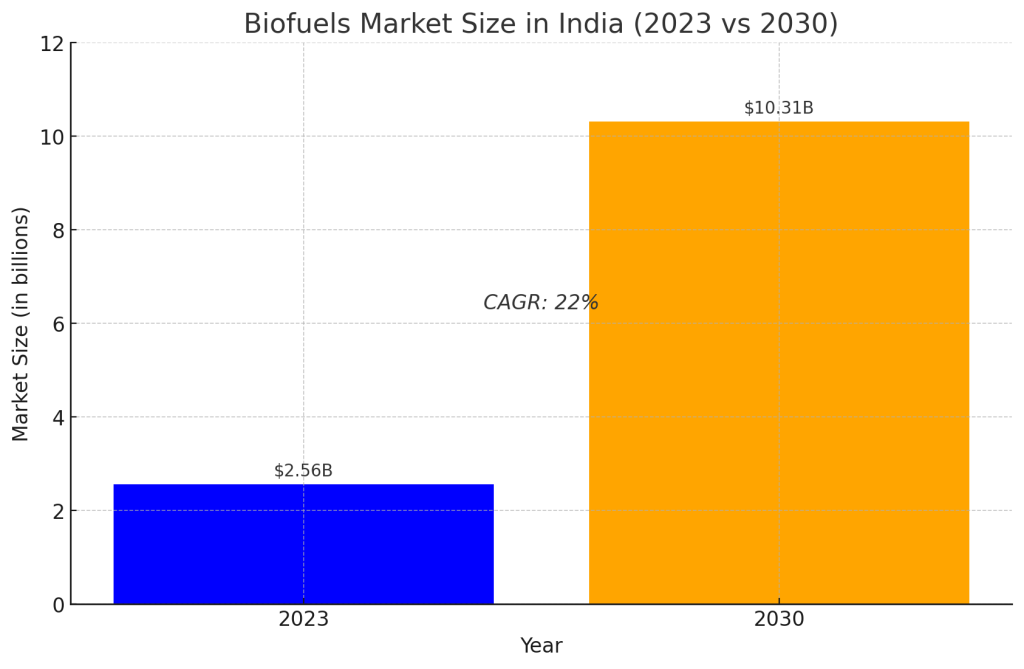

Total Biofuels Market Size in India:

- Current Market Size: The biofuels market in India was valued at approximately $2.56 billion in 2023.

- Market Size Projection by 2030: It is estimated to grow to $10.31 billion by 2030, representing a CAGR of 22%.

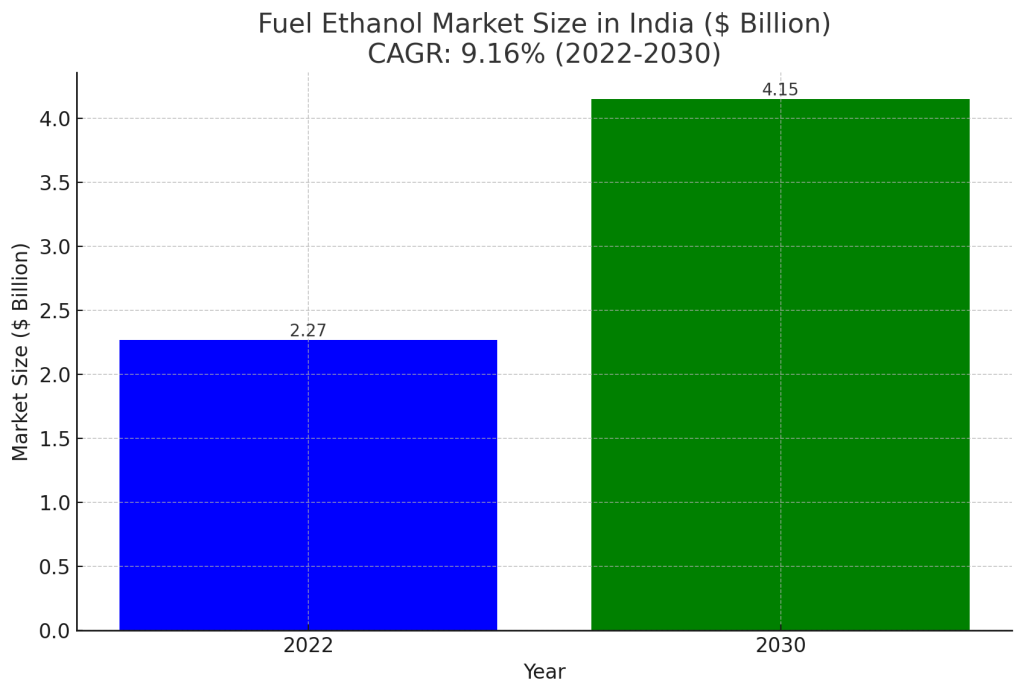

Total Market Size for Fuel Ethanol in India:

- Current Market Size: The fuel ethanol market in India stands at $2.27 billion in 2022

- Market Size Projection by 2030: It is expected to reach $4.15 Billion by 2030, with a compound annual growth rate (CAGR) of 9.16%.

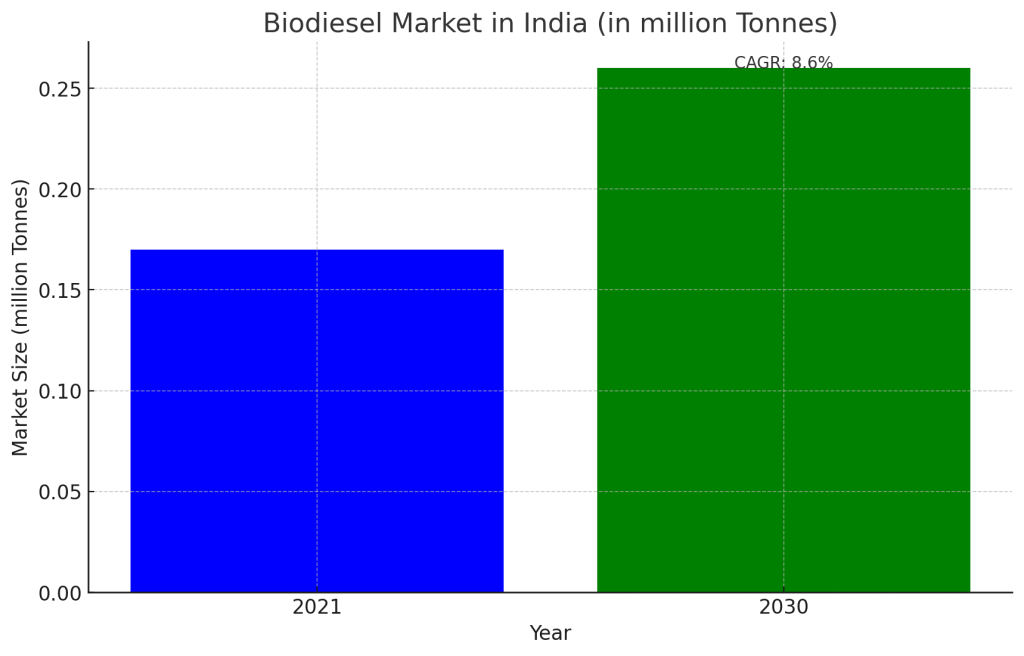

Total Market Size for Biodiesel in India:

- The biodiesel market in India is valued at 0.17 million Tonnes in 2021.

- Market Size Projection by 2030: It is anticipated to increase to 0.26 million Tonnes by 2030, reflecting a CAGR of 8.60%.

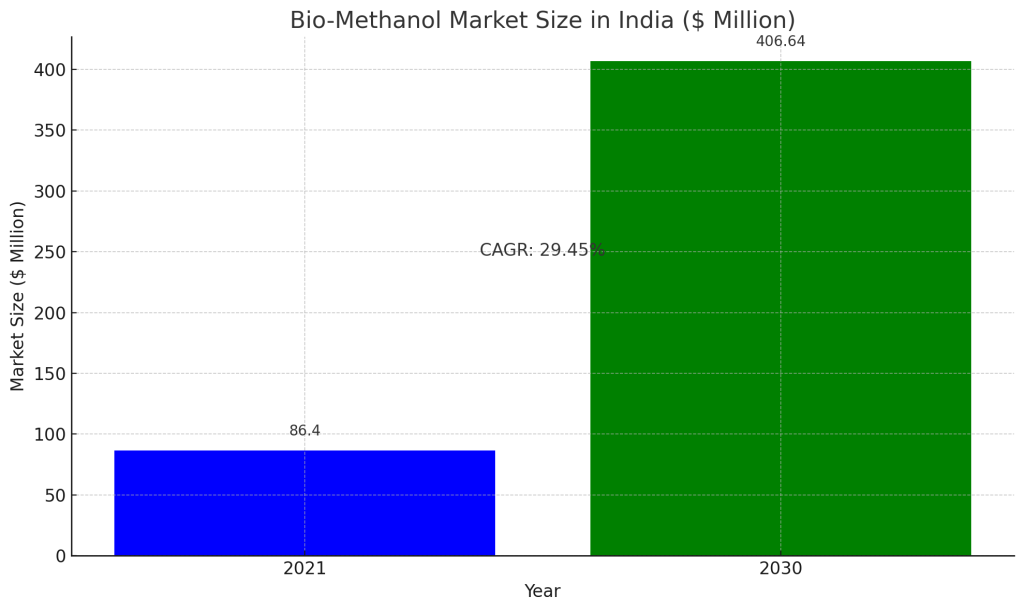

Total Market Size for Bio-methanol in India:

- Current Market Size: The bio-methanol market in India is valued at $86.4 Million in 2021.

- Market Size Projection by 2030: It is forecasted to grow to $406.64 by 2030, at a CAGR of 29.45%.

Key Indian Players in the Indian Ethanol Market:

- Indian Oil Corporation Limited (IOCL): IOCL is one of the largest oil and gas companies in India and plays a significant role in the ethanol market.Indian Oil Corporation Limited has firmed up plans to set up two ethanol plants in Telangana and Andhra Pradesh at about RS 600 crore each. The company has received approvals from Telangana which has suggested two sites for the ethanol plant.

- Bharat Petroleum Corporation Limited (BPCL): BPCL along with OMCs has signed 131 LTOAs with project proponents proposing to set up ethanol plants of approx. 757 Cr lit per annum capacity in ethanol deficit states. BPCL is setting up an integrated 2G and 1G Bio Ethanol Refinery at Bargarh, Odisha. The Bioethanol Refinery, which will increase the production capacity to about 6 Cr lit per annum of ethanol.

- Hindustan Petroleum Corporation Limited (HPCL): HPCL, like IOCL and BPCL, is a state-owned oil and gas company with interests in ethanol blending and distribution.Hindustan Petroleum Corporation (HPCL) is investing over ₹14 billion (~$168.12 million) to build a Second Generation (2G) bio-refinery plant in Bathinda, Punjab, using paddy straw to produce ethanol as part of the government’s Ethanol Blending Program (EBP).

- Praj Industries Limited: Praj Industries has bagged an order to set up India’s largest capacity syrup based ethanol plant from Godavari Biorefineries (GBL) in Karnataka. As a part of this project, Praj Industries will expand the existing ethanol manufacturing capacity to 600 kilo litre per day (KLPD), using sugarcane syrup. When commissioned, this will become India’s largest capacity syrup-based ethanol plant.

- Rajasthan State Ganganagar Sugar Mills Limited (RSGSM): RSGSM is a state-owned sugar mill in Rajasthan that is actively involved in ethanol production and supplies ethanol to oil marketing companies for blending with petrol.

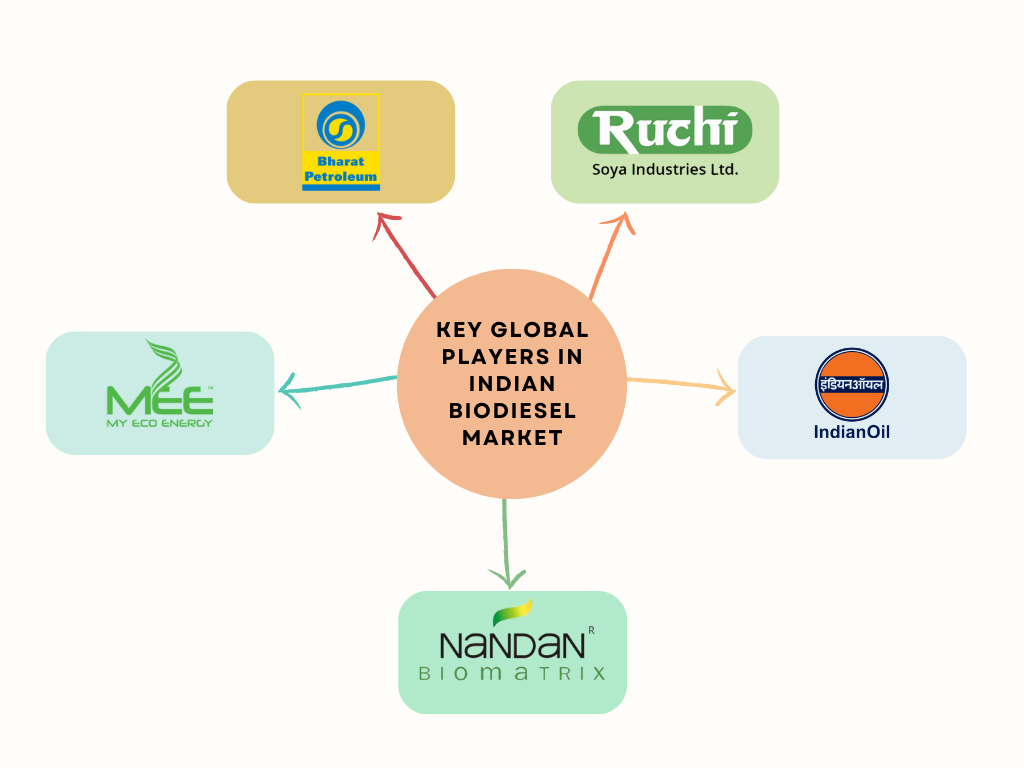

Key Indian Players in the Indian Biodiesel Market:

- Indian Oil Corporation Limited (IOCL): Indian Oil has issued 23 LOIs for biodiesel plants with a total capacity of 557.57 tonnes per day, the statement added. The firm has received 51 kilolitres of biodiesel made from used cooking oil at its Tikrikalan terminal in Delhi. It has also started constructing eight biodiesel plants across Uttar Pradesh, Gujarat, and Madhya Pradesh.

- Bharat Petroleum Corporation Limited (BPCL): BPCL is another major state-owned oil and gas company in India that is active in the biodiesel sector. A total of nine Expressions of Interest (EOIs) with a combined capacity of 138 TPD (tons per day) have been issued by BPCL, which has also begun generating biodiesel from used cooking oil. As of March 2022, four LOIs with a combined production capacity of 85 TPD have been granted.

- Ruchi Soya Industries Limited: Ruchi Soya is one of the largest producers of edible oils in India and is also active in the biodiesel market. The company produces biodiesel from non-edible oilseeds such as Jatropha and Pongamia. Leading soya producer ‘Ruchi Soya Industries Ltd’ and public sector oil major IndianOil have signed a limited liability partnership (LLP) agreement to undertake jatropha plantation in Uttar Pradesh for manufacturing biofuel. The two partners have agreed to form a separate joint venture IndianOil-Ruchi Biofuels LLP at a project cost of Rs 436.63 crore. A major part of the project cost will be funded by the government of Uttar Pradesh under the National Rural Employment Guarantee Scheme.

- My Eco Energy Pvt. Ltd.: My Eco Energy is all set to establish its foothold in the Indian Fuel Industry with the launch of its all-new revolutionary product INDIZEL. Indizel is a unique clean diesel fuel introduced in the Indian Market which meets European (EN 590 EURO 6 ), and BIS ( IS 1460 ) Bharat stage VI strictest fuel quality parameters collating with World Wide Fuel Charter ( WWFC – Worldwide Fuel Charter ), category 4 requirements. This sulfur-free, aromatics-free and virtually odourless fuel can achieve up to 80% reduction in greenhouse gas emissions compared to petroleum diesel, making it the next big thing in the Indian fuel industry.

- Nandan Biomatrix Limited: Nandan Biomatrix along with Bharat Petroleum Corporation and Shapoorji & Pallonji formed a joint venture company for producing bio-diesel from jatropha in Uttar Pradesh. The JV company, registered it in Lucknow, is awaiting the UP government approval for the proposed project. The total cost of the project is estimated to be about Rs.2,000 crore. While Nandan proposes to set up its own R&D centre in Kanpur, clonal stations for multi-propagation methods besides providing training to the farmers

- Godrej Agrovet Limited: Godrej Agrovet and Ruchi Soya Industries Limited are two companies that have shown interest in producing biodiesel from non-edible oilseeds. Furthermore, businesses producing biodiesel have benefited from government efforts like the National Mission on Biodiesel and Biodiesel Purchase Policy.

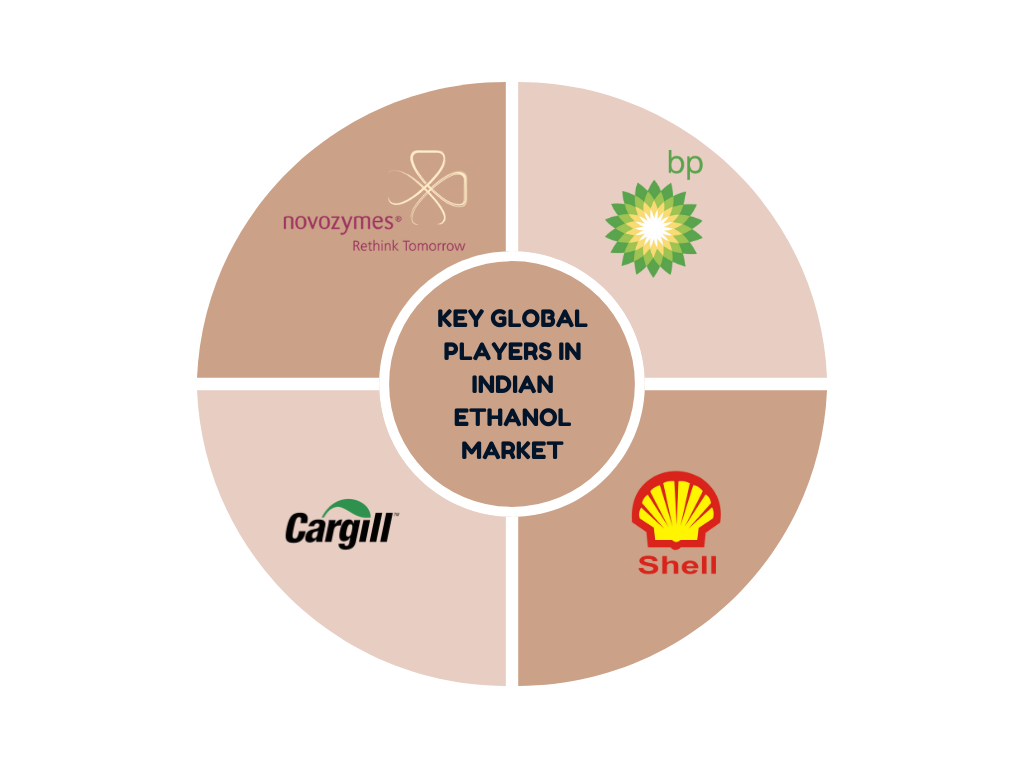

Key International Players in the Indian Ethanol Market:

- Novozymes: Indian process and project engineering specialist Praj Industries is to build a demonstration biofuel plant using enzymes supplied by a local unit of Danish Novozymes. The enzymes will help in the process of turning wheat straw, rice straw, bagasse and other sources of biomass into fuels such as ethanol, Novozymes South Asia’s head G S Krishnan explained. Novozymes has already formed a partnership with Indian biotech start-up Sea6 Energy to develop a seaweed-to-fuel production process. The company is interested in additional partnerships on biofuel research

- BP (British Petroleum): BP, a British multinational oil and gas company, has been exploring opportunities in the Indian ethanol market as part of its renewable energy strategy. Jio-bp, the fuel and mobility joint venture of Reliance Industries Ltd and UK’s bp, has launched petrol blended with 20 percent ethanol, aligning with the government programme to cut oil imports and reduce carbon emissions.”In line with the roadmap set by the Government, Jio-bp has become one of the first fuel retailers in India to make E20 blended petrol available,” the company said in a statement.

- Shell: Royal Dutch Shell, a multinational oil and gas company, has been involved in biofuel research and development globally. A catalyst being developed by Shell Technology Centre Bangalore (STCB), one of the three tech hubs of Shell besides the ones in Houston and Amsterdam, holds out the promise of converting agricultural and municipal waste into liquid transport fuel. India produces 60 billion tonnes of municipal waste and 200 million tonnes of agricultural waste every year. If the experiment succeeds and is commercialised, it could generate 60-80 million tonnes of biofuel and meet a large part of India’s energy needs.

- Cargill: Cargill, an American multinational corporation. Cargill India is keen to invest in facilities to produce ethanol out of corn but would wait for a clear policy on the green fuel, as the current schemes of the government are skewed in favour of sugar mills. The company would take a call after assessing how attractive is the ethanol policy once it is announced.

Key International Players in the Indian Biodiesel Market:

- Wilmar International Limited: Wilmar International is a Singapore-based agribusiness company and one of the largest palm oil producers globally. The company has a presence in India and is involved in the production and distribution of biodiesel derived from palm oil.

- Cargill: Cargill is an American multinational corporation involved in various industries, including agriculture and biofuels. The company has operations in India and may be involved in the production and distribution of biodiesel, particularly from edible oil feedstocks.

- Bunge Limited: Bunge Limited is an American agribusiness and food company with global operations. While they may not have a direct presence in the Indian biodiesel market, they are involved in the production and trading of vegetable oils, which can be used as feedstocks for biodiesel production.

- ADM (Archer Daniels Midland): ADM is an American global food processing and commodities trading corporation with interests in biofuels. While they may not have direct involvement in the Indian biodiesel market, they have operations in India and may supply feedstocks or technology for biodiesel production.

- BASF: BASF is a German multinational chemical company involved in various industries, including renewable energy. While they may not have a direct presence in the Indian biodiesel market, they provide catalysts and technologies for biodiesel production globally.

- Louis Dreyfus Company: Louis Dreyfus Company is a global merchant and processor of agricultural goods, including oilseeds. While they may not have a direct presence in the Indian biodiesel market, they are involved in the trading and processing of vegetable oils, which can be used as feedstocks for biodiesel production.

- Ventura Olmeca Group: Ventura Olmeca Group is a Spanish company specializing in the production of biodiesel from various feedstocks, including waste cooking oil. They have operations in India and are involved in the production and distribution of biodiesel in the country.

Government Policies for Fuel Ethanol:

| Policy/Program | Year Introduced | Description |

|---|---|---|

| National Biofuel Policy (NBP) 2018 | 2018 | Promotes the production and use of biofuels, including ethanol. Allows surplus food grains for ethanol production for blending with petrol. |

| Ethanol Blended Petrol (EBP) Program | 2003 | Introduces ethanol blending in petrol with objectives like reducing import dependence, saving foreign exchange, boosting domestic agriculture, and environmental benefits. |

| Flexible Ethanol Blending Program | 2021 | Allows flexible ethanol blending with petrol to use surplus ethanol, facilitating higher blending targets. Gives flexibility to oil marketing companies. |

| Sugarcane Price Policy | 2023 | Sets Fair and Remunerative Price (FRP) for sugarcane. Encourages sugar mills to divert sugarcane for ethanol production by providing incentives and subsidies. |

| Ethanol Procurement Policy | 2014 | Ensures procurement of ethanol by oil marketing companies for blending with petrol. Provides framework for ethanol procurement, pricing, and quality standards. |

Government Policies for Biodiesel:

| Initiative | Description |

|---|---|

| National Biodiesel Mission (NBM) | Launched by the Government of India to promote the production of biodiesel from non-edible oilseed crops. Aims to enhance energy security, promote sustainable agriculture, and reduce greenhouse gas emissions. Focuses on cultivation of non-edible oilseed crops such as Jatropha, Pongamia, and Karanja. |

| Biodiesel Purchase Policy | Implemented by the Indian government to encourage the use of biodiesel. Encourages various government departments and agencies to procure biodiesel for transportation and other needs. Provides incentives and subsidies to biodiesel producers and users. |

| Minimum Support Price (MSP) for Non-Edible Oilseeds | Sets Minimum Support Prices for various agricultural crops, including non-edible oilseeds like Jatropha and Pongamia. Ensures farmers receive a fair price for their produce, encouraging the cultivation of non-edible oilseed crops for biodiesel production. |

Key Challenges Faced by the Indian Ethanol Market:

- Feedstock Availability and Price Volatility: The availability and price volatility of feedstocks such as sugarcane, molasses, and grains pose a significant challenge to ethanol production in India. Fluctuations in agricultural production, weather conditions, and market demand can affect feedstock availability and prices, impacting the viability and profitability of ethanol production.

- Infrastructure Constraints: Limited infrastructure for ethanol production, storage, transportation, and distribution is a major challenge in the Indian ethanol market. Insufficient storage facilities, inadequate transportation networks, and lack of blending infrastructure hinder the efficient supply and distribution of ethanol to end-users, including fuel retailers.

- Regulatory Hurdles: Regulatory hurdles related to permits, licenses, and approvals for ethanol production and blending can create barriers for market entry and expansion. Complex regulatory frameworks, bureaucratic processes, and delays in obtaining necessary approvals can impede the growth of the ethanol industry in India.

- Ethanol Pricing and Subsidy Mechanism: The pricing mechanism for ethanol, including procurement prices set by the government and subsidies provided to ethanol producers, can impact the competitiveness and profitability of ethanol production. Uncertainty surrounding ethanol pricing and subsidy disbursement creates challenges for ethanol producers and investors in planning and decision-making.

- Technological Challenges: Technological challenges related to ethanol production processes, including low conversion efficiencies, high energy consumption, and limited scalability of production technologies, pose barriers to the widespread adoption of ethanol as a fuel in India. Research and development efforts are needed to address these challenges and improve the efficiency and cost-effectiveness of ethanol production technologies.

- Market Demand and Consumer Awareness: Limited market demand for ethanol-blended fuels, coupled with low consumer awareness and acceptance of ethanol as a fuel, is a challenge in the Indian ethanol market. Increasing consumer awareness about the benefits of ethanol-blended fuels and creating demand through promotional campaigns and incentives are necessary to stimulate market growth.

- Policy and Regulatory Environment: Inconsistent and changing government policies, including ethanol blending targets, procurement prices, and subsidy schemes, create uncertainty and risk for ethanol producers and investors. A stable and supportive policy and regulatory environment is essential to foster long-term investment and growth in the ethanol market.

Key Challenges Faced by the Indian Biodiesel Market:

- Feedstock Availability and Price Volatility: The availability and price volatility of feedstocks such as non-edible oilseeds (e.g., Jatropha, Pongamia, Karanja), waste cooking oil, and animal fats pose a significant challenge to biodiesel production in India. Fluctuations in agricultural production, weather conditions, and market demand can affect feedstock availability and prices, impacting the viability and profitability of biodiesel production.

- Land Use and Competition with Food Crops: The cultivation of non-edible oilseed crops for biodiesel production competes with food crops for agricultural land, water, and resources. This competition raises concerns about food security, land use change, and environmental sustainability, posing challenges to the expansion of biodiesel production in India.

- Infrastructure Constraints: Limited infrastructure for biodiesel production, storage, transportation, and distribution is a major challenge in the Indian biodiesel market. Insufficient processing facilities, inadequate storage capacity, and lack of distribution networks hinder the efficient supply and distribution of biodiesel to end-users, including transportation and industrial sectors.

- Technological Challenges: Technological challenges related to biodiesel production processes, including low conversion efficiencies, high energy consumption, and limited scalability of production technologies, pose barriers to the widespread adoption of biodiesel as a fuel in India. Research and development efforts are needed to address these challenges and improve the efficiency and cost-effectiveness of biodiesel production technologies.

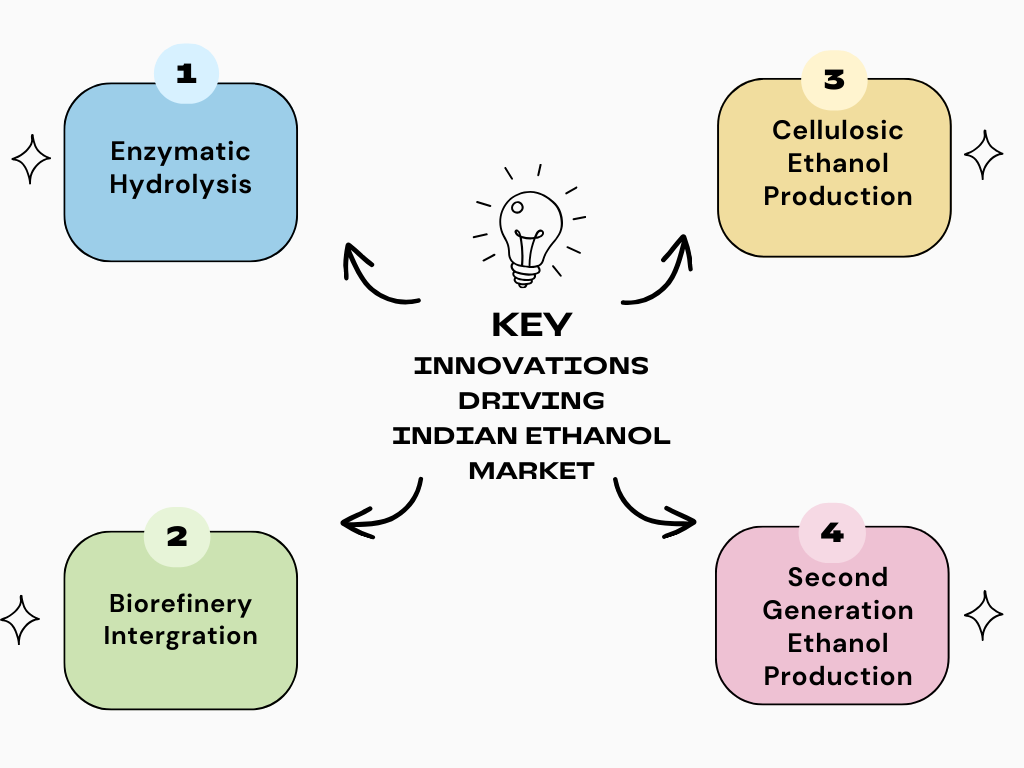

Key Innovations Driving the Indian Ethanol Market:

- Advanced Biofuel Technologies: Innovations in biofuel production technologies are driving efficiency improvements and cost reductions in ethanol production. Advanced biofuel technologies, such as enzymatic hydrolysis, fermentation optimization, and cellulosic ethanol production, are enabling the use of diverse feedstocks, including agricultural residues, lignocellulosic biomass, and waste materials, for ethanol production.

- Biorefinery Integration: Integration of ethanol production with biorefinery concepts is driving innovation in the Indian ethanol market. Biorefineries enable the conversion of various biomass feedstocks into multiple value-added products, including ethanol, biodiesel, biogas, biochemicals, and biomaterials, maximizing resource utilization and revenue generation.

- Second-Generation Ethanol Production: Innovations in second-generation ethanol production technologies are enabling the commercial-scale production of ethanol from lignocellulosic biomass, such as agricultural residues (e.g., rice straw, wheat straw, corn stover) and energy crops (e.g., switchgrass, miscanthus). Second-generation ethanol production processes, including biochemical and thermochemical conversion routes, are overcoming technical challenges and scaling up to commercial production levels.

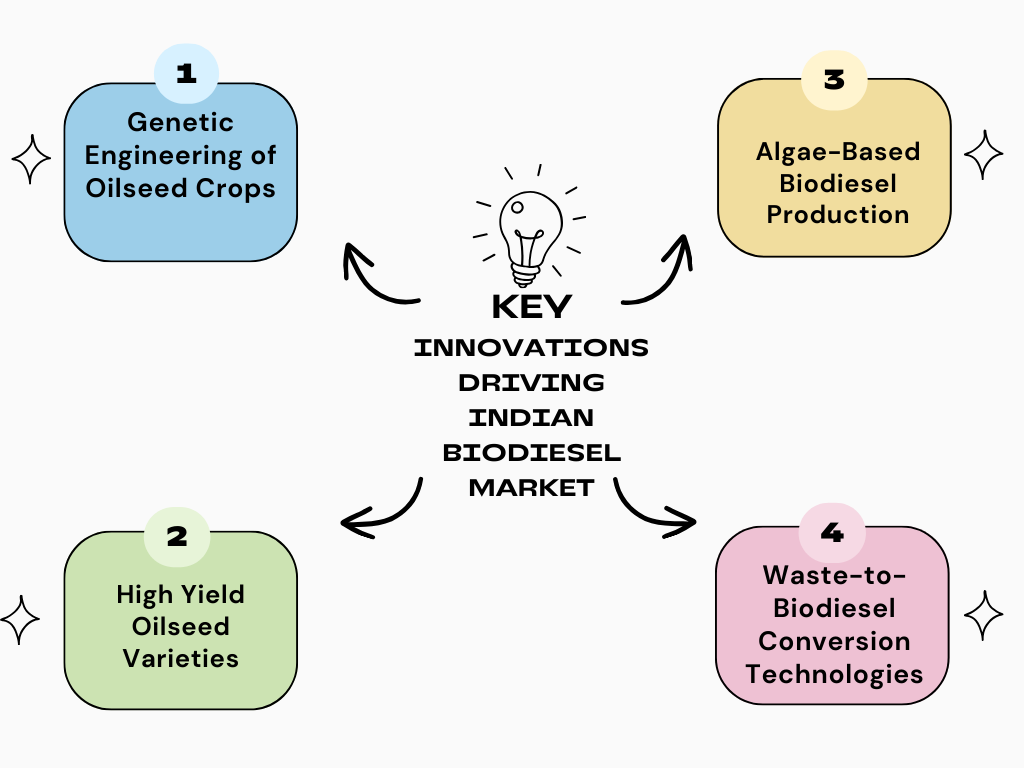

Key Innovations Driving the Indian Biodiesel Market:

- Advanced Feedstock Cultivation Techniques: Innovations in agricultural practices and crop cultivation techniques are driving improvements in feedstock yields and quality for biodiesel production. Advanced farming methods, including precision agriculture, genetic engineering, and biotechnology, enable the cultivation of high-yielding oilseed crops suitable for biodiesel production, such as Jatropha, Pongamia, and Karanja.

- Genetic Engineering of Oilseed Crops: Genetic engineering and biotechnological innovations are driving improvements in oilseed crops for biodiesel production. Genetic modification techniques enable the development of oilseed crops with enhanced oil content, stress tolerance, and agronomic traits, leading to increased biodiesel yields and productivity.

- High-Yield Oilseed Varieties: Breeding and selection of high-yielding oilseed varieties with improved oil content, seed characteristics, and agronomic traits are driving innovation in the Indian biodiesel market. Development and commercialization of high-yield oilseed varieties suitable for biodiesel production contribute to increased feedstock availability and sustainability.

- Waste-to-Biodiesel Conversion Technologies: Innovations in waste-to-biodiesel conversion technologies are enabling the utilization of various organic waste streams for biodiesel production. Advanced conversion processes, including transesterification, esterification, and pyrolysis, convert waste oils, animal fats, and grease trap waste into biodiesel, reducing waste disposal and environmental pollution.

- Algae-based Biodiesel Production: Research and development in algae-based biodiesel production technologies are driving innovation in the Indian biodiesel market. Algae cultivation systems, photobioreactors, and downstream processing techniques enable the production of biodiesel from microalgae, offering high oil yields, fast growth rates, and potential for wastewater treatment and carbon sequestration.

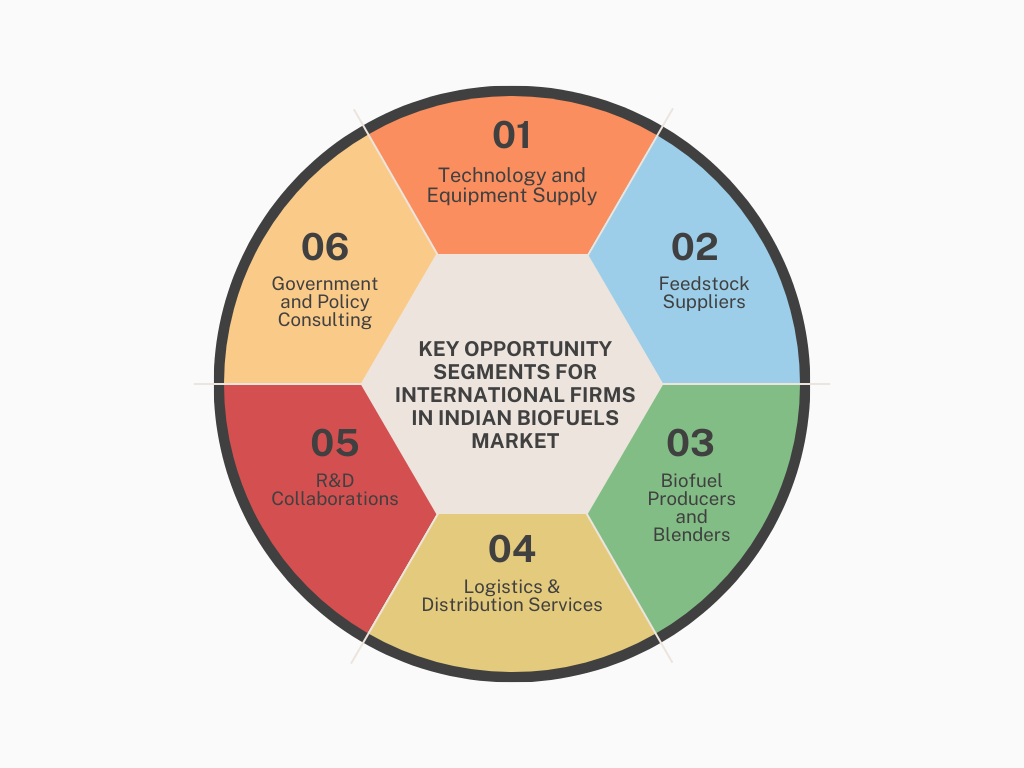

Key Opportunity Segments for International Firms in the Indian Biofuels Market:

- Technology and Equipment Providers: International firms specializing in biofuel production technologies, equipment, and machinery have opportunities to provide innovative solutions to Indian biofuel producers. This includes technologies for biomass conversion, fermentation, distillation, and purification, as well as equipment for biofuel plants and biorefineries.

- Feedstock Suppliers: International firms involved in the supply of biofuel feedstocks such as non-edible oilseeds, agricultural residues, waste oils, and algae biomass can tap into the Indian market. They can establish partnerships with local farmers, cooperatives, and agribusinesses to ensure a sustainable and reliable supply chain for biofuel production.

- Biofuel Producers and Blenders: International biofuel producers and blenders have opportunities to enter the Indian market and collaborate with local partners to produce and distribute biofuels such as biodiesel and ethanol. They can leverage their expertise, technologies, and experience to enhance production efficiency, product quality, and market penetration.

- Research and Development (R&D) Collaborations: International firms specializing in biofuel research, development, and innovation can collaborate with Indian research institutions, universities, and companies to advance biofuel technologies and solutions. R&D collaborations can focus on improving feedstock productivity, enhancing conversion processes, and developing sustainable biofuel production pathways.

- Logistics and Distribution Services: International firms offering logistics, transportation, and distribution services for biofuels have opportunities to support the efficient supply chain management of biofuels in India. This includes transportation of feedstocks, intermediate products, and finished biofuels from production facilities to distribution points and end-users.

- Government and Policy Consulting: International firms specializing in government relations, policy analysis, and consulting services can assist biofuel stakeholders in navigating regulatory frameworks, accessing incentives, and complying with sustainability standards. They can provide strategic advice and advocacy support to shape biofuel policies and regulations in India.

- Investment and Financing: International financial institutions, venture capital firms, and private equity investors can explore investment opportunities in Indian biofuel projects and companies. They can provide capital, funding, and financial expertise to support biofuel infrastructure development, technology adoption, and market expansion in India.

Conclusion:

The Indian biofuels market is appealing for international investment because of its growing energy needs, ample biomass resources, supportive government policies, and expanding market. With India’s focus on renewable energy and favorable regulations, international investors can help develop sustainable biofuel infrastructure. Collaborations with Indian firms also offer opportunities for innovation and market growth, making India a promising destination for investment in renewable energy.