Strategic Insights Report: Sustainable Aviation Fuel

About Us

Energy Alternatives India (EAI)

India’s leading catalyst for climate tech since 2008.

▶ Domains: Renewable energy | Low-carbon mobility | Sustainable materials | Clean environment

▶ Services:

• Strategic & market intelligence

• Startup & innovation ecosystem support

• Geo-targeted decarbonization solutions

Our specialty focus areas include

Our specialty focus areas include

Net Zero by Narsi

Insights and interactions on climate action by Narasimhan Santhanam, Director - EAI

View full playlist▶ Track Record: Solar, biomass, decarbonization, biofuels, green chemicals and more.

→ Powering India’s sustainable growth & climate action

→ Assisted 100+ companies including JSW Energy, ExxonMobil, Vedanta, GE, GSW…

INDEX

- Executive Summary

- Introduction to SAF

- The Need and Key Drivers

- Value chain and Components

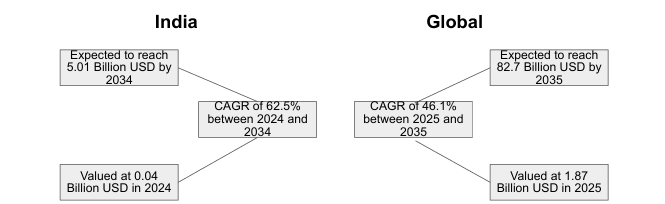

- Market Size

- Policies, Reputation & Financial Incentives

- Technologies and Recent Innovations

- Business Models

- Strategic Landscape

- Risk and Mitigation

- Call to Action

EXECUTIVE SUMMARY

“India’s aviation sector is on track to triple by 2040. Sustainable Aviation Fuel (SAF) is the billion-rupee opportunity that enables decarbonization while offering long-term cost and carbon advantages to airlines.”

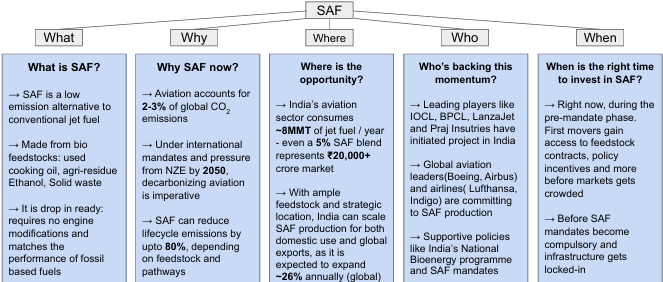

INTRODUCTION TO SAF

Sustainable Aviation Fuel (SAF) is a low-carbon jet fuel made from renewable feedstocks, capable of powering existing aircraft engines with blends up to 50%.

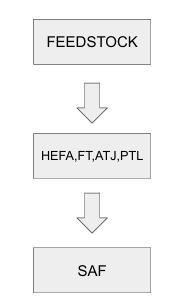

The primary feedstock involves:

→ used cooking oil, agricultural residues, municipal solid waste, industrial waste gases (including CO₂), algal oil, cellulosic ethanol

Conversion pathways include:

• Fischer Tropsch (FT)

• Alcohol to Jet (ATJ)

• Hydroprocessed Esters and Fatty Acids (HEFA)

• Power to liquid (PTL)

• Co-processing of bio-feedstocks at oil refineries

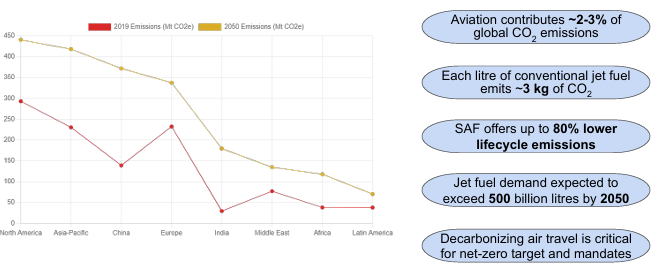

THE NEED AND KEY DRIVERS

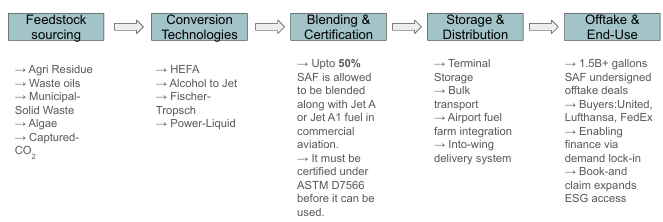

VALUE CHAIN AND COMPONENTS

The SAF value chain spans five core segments, each with its own growth dynamics and investment attractiveness.

PROJECTED GROWTH IN THE FUTURE

• The Global Aviation Fuel consumption is about ~295Mt per year in which commercial aviation alone accounts for 80 – 90% of this usage.

• With a humongous production in the biomass, estimated to be 130 million metric tonnes per year, converting the aviation industry completely to SAF is possible in the mere future.

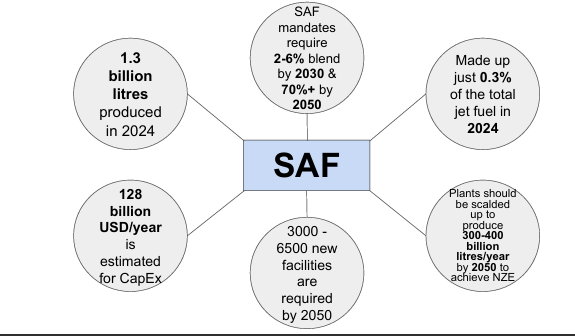

PRODUCTION AND CAPACITY (GLOBAL)

POLICIES & REPUTATION

National SAF Policy Framework (Upcoming)

• A dedicated SAF policy roadmap is being jointly developed by:

○ Ministry of Civil Aviation (MoCA)

○ Ministry of Petroleum & Natural Gas (MoPNG)

○ NITI Aayog

• This policy will define:

○ Blending mandates (starting with 1% by 2027)

○ Feedstock flexibility (bio-based, municipal waste, lignocellulosic, PtL)

○ Incentive structures to reduce SAF’s cost premium

| TARGET YEAR | SAF BLEND | ESTIMATED VOLUME |

|---|---|---|

| 2027 | 1% | ~120 Mn Litres |

| 2028 | 2% | ~250 Mn Litres |

| 2030 | 5% | ~600 Mn Litres |

| 2035 | 10%+ | 1+ Bn Litres |

At ₹110/litre SAF price, total SAF market =

→ ₹715 crore – 2027

→ $900M+ market in 10 years

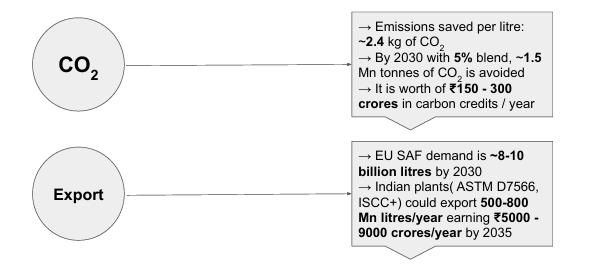

CARBON CREDITS & EXPORT POTENTIAL

RECORDED SAF INVESTMENTS

| Investor | Technology | Investment Size | Capacity | Location |

|---|---|---|---|---|

| Indian Oil & LanzaJet JV | ATJ | IOCL – ₹1500 Cr Lanzajet – ₹750 Cr Airlines – ₹750 Cr |

85,000t/year | Haryana |

| BPCL | HEFA, ATJ, Co-processing | ₹1400 Cr | 100t/day by 2027 | Mumbai, Kochi |

| MRPL | HEFA (UCO/Palm stearin) | ₹450 Cr | 20kL/day | Mangalore |

| Thyssenkrupp India | Unspecified | ₹3000 Cr | Similar to IOCL | Various locations in India |

| NTPC | Multiple Pathways | Part of $50 B clean energy plans | 100,000t/year | Andhra Pradesh |

FINANCIAL INCENTIVES

COST GAP & FUNDING REQUIRED

→ SAF price today: ₹110 – 160 / litre

→ Jet A1 price: ₹75 – 90 / litre (2024)

→ Cost Gap: ₹35 – 70 / litre

For 1% blend → Govt viability gap funding (VGF) needed is: ₹420 – 840 Cr / year

VGF under discussion:

• ₹30 – 50 / litre support

• Would reduce investor risk during first 5 – 7 years of scale up

FINANCIAL SUPPORT UNDER EVALUATION

→ Viability Gap Funding (VGF): ₹30 – 50 / litre SAF cost bridge

→ MNRE bioenergy scheme: CapEx subsidies up to 35% for eligible tech

→ IREDA/SIDBI: Offers green bonds, low interest SAF project loans

→ Project Sector Lending: SAF is now included under green finance

TECHNOLOGY AND RECENT INNOVATIONS

| S.NO | Pathway | Feedstock | CapEx ($/L) | OpEx ($/L) | Market Price ($/L) | Conversion Efficiency | Tech Maturity |

|---|---|---|---|---|---|---|---|

| 1 | HEFA | Used cooking & vegetable oil | ~$1.8-2.5 | $1.2-1.5 | $1.6-2.0 | ~80% | 9 (Commercial) |

| 2 | ATJ | Ethanol, butanol | ~$2.5-4.0 | $2.2-2.6 | $2.7-3.2 | ~45-55% | 7-8 (Demo) |

| 3 | FT-SPK | Biomass, municipal solid waste | ~$3.5-5.0 | $2.0-2.4 | $2.5-3.0 | ~35-40% | 7-8 (Demo) |

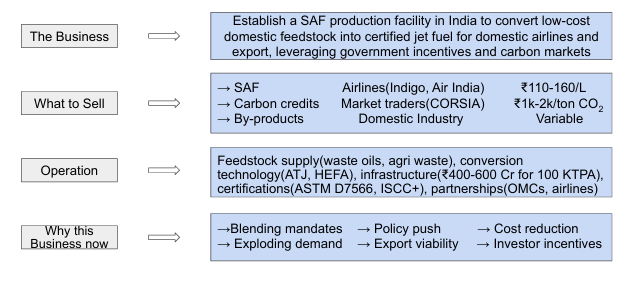

BUSINESS MODEL

EXAMPLE FOR A 100 KTPA PLANT

| Metric | Value |

|---|---|

| Annual SAF Output | 120 million litres |

| Avg Selling Price (blended) | ₹125/litre |

| Gross Revenue | ₹1,500 crore/year |

| Carbon Credit Income | ₹150–250 crore/year |

| OPEX (incl. feedstock) | ₹900–1,000 crore/year |

| EBITDA Margin | 25–30% (with policy support) |

| Break-even Period | 5–7 years |

GLOBAL BENCHMARKING

| COUNTRY | SAF PRODUCERS | ANNUAL CAPACITY |

|---|---|---|

| USA | World Energy, Neste, LanzaJet | ~700 KTPA |

| EU | TotalEnergies, Neste | ~600 KTPA |

| SINGAPORE | Neste (World’s largest SAF plant) | 1000 KTPA |

| INDIA | Emerging (No commercial SAF output) | < 5 KTPA |

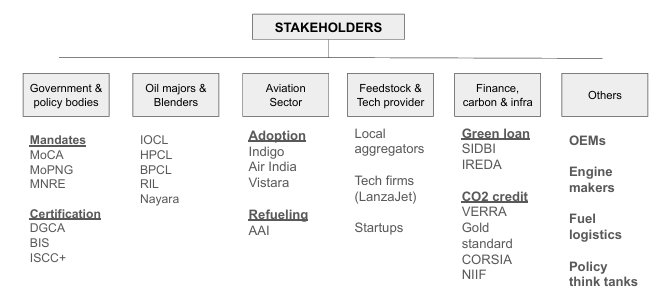

STAKEHOLDERS IN INDIA’S SAF ECOSYSTEM

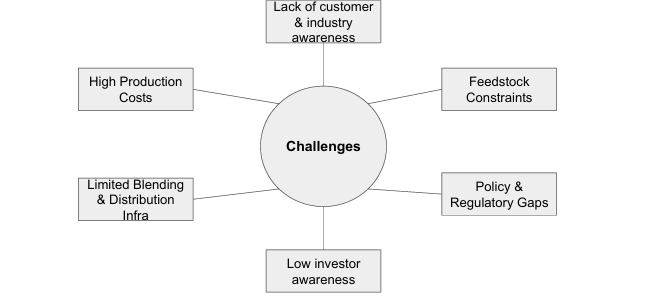

KEY CHALLENGES

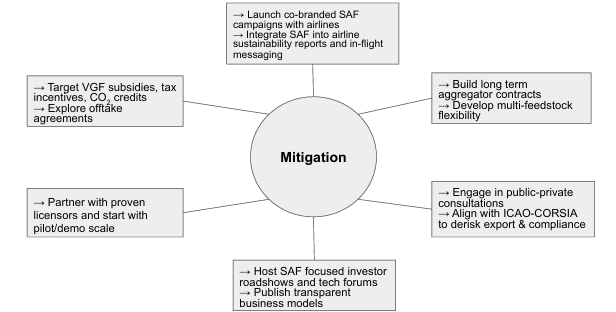

SOLUTIONS

MOVING FORWARD

- India’s aviation market is expected to double by 2035, driving significant demand for sustainable aviation fuel (SAF).

- The country has abundant access to low-cost feedstocks such as used cooking oil, agricultural residue, and municipal waste, making it ideal for SAF production.

- Currently, there is no commercial-scale SAF output in India, offering a strong first-mover advantage to early investors.

- International markets like the EU and UK already have SAF blending mandates in place, opening up immediate export opportunities.

- Government support is growing through incentives like viability gap funding, carbon credits, and green financing frameworks.

- The combination of policy momentum, global demand, and domestic resource readiness makes now the right time to invest in India’s SAF ecosystem.

WHY PARTNER WITH EAI?

- We are India’s leading clean-tech consulting firm with 15+ years of expertise in renewable energy, biofuels, and climate tech.

- Deep understanding of SAF pathways (HEFA, ATJ, EtJ, PtL) and active involvement in national-level SAF dialogues and policy forums.

- Strong network across feedstock aggregators, biofuel startups, PSUs, and international licensors, enabling seamless value chain integration.

- Proven track record in supporting technology commercialization, go-to-market strategy, and investor relations for climate-tech ventures.

- Access to exclusive market intelligence and feasibility databases, helping de-risk decisions and accelerate scale-up.

Wish to have industry or market research support from specialists for climate & environment? Talk to EAI team – Call Muthu at +91-9952910083 or send a note to consult@eai.in

India Big Business Opportunities in Climate Tech – List – EAI

India Big Business Opportunities in Climate Tech – List – EAI